After a challenging period of elevated rates, Europe's leveraged finance markets are poised for growth in 2025, with stabilising costs, rising competition and renewed opportunities for dealmakers.

European leveraged finance markets back on track

European leveraged finance markets rallied strongly in 2024, with momentum for new deals and opportunities for borrowers and lenders alike in 2025

Europe's leveraged finance markets enter 2025 following a solid performance in 2024, with the syndicated loan and high yield bond markets rallying and private debt remaining active. European loan and bond issuance nearly doubled year-on-year. Refinancing and repricing drove activity, as issuers returned to the market to take advantage of lower interest rates and bring down borrowing costs. With base rates falling, investors with a renewed appetite for yield have been eager to provide their support.

Moreover, with the revival of the loan and bond markets, borrowers have jumped at the opportunity to push out maturities and lower financing costs, and have in some cases taken the opportunity to refinance pricier unitranche structures provided by private debt players with cheaper loan and bond options.

This has created a fluid market where quality borrowers have had a broader range of products to choose from and the ability to select the best possible financing options to match their specific requirements.

Although public debt markets have regained market share, private debt players remain as relevant and active as ever, with their ability to price risk and deliver rapid deal execution.

With all the lending channels open again, the competitive dynamic between public and private debt providers has intensified to the benefit of the borrowers. Private debt players have tightened margins and offered more covenant flexibility to win new business. Public debt markets have sharpened execution and broadened the types of facilities they offer.

The only missing piece of the puzzle in 2024 has been a steady pipeline of new M&A and leveraged buyout financing opportunities.

This has been more of a function of an only moderately improving M&A deal market than a lack of investor and lender appetite. However, there is a growing optimism that deal activity will grow within the next 12 months, as interest rates come down and vendors and buyers align on valuation.

If and when the M&A market picks up, financing markets will be well positioned to support dealmakers.

European leveraged finance overview

Leveraged finance markets rallied in 2024 to record remarkable year-on-year gains

Interest rate cuts and tighter margins generated a surge in refinancing, as borrowers leapt at the chance to bring down financing costs

Bumper CLO issuance drove demand, with investors seeking yield as rates came down

A dynamic interplay between private debt and public debt continues to develop, with the two markets competing and, in some instances, collaborating

As rates fluctuate, private debt managers must adapt their investment strategies and risk management practices to navigate changing market conditions

Despite increased competition, private debt's ability to provide flexible solutions and focus on deep borrower relationships, and its active portfolio management, still set it apart from traditional lending

As the industry matures, strategic alliances between banks and private debt funds are slowly emerging to expand market reach

Falling interest rates have been the primary catalyst for the market’s revival, with both the European Central Bank and Bank of England making interest rate cuts in 2024 for the first time in two and twoand- a-half years, respectively

Leveraged finance markets rallied in 2024 to record remarkable year-on-year gains

Interest rate cuts and tighter margins generated a surge in refinancing, as borrowers leapt at the chance to bring down financing costs

Bumper CLO issuance drove demand, with investors seeking yield as rates came down

A dynamic interplay between private debt and public debt continues to develop, with the two markets competing and, in some instances, collaborating

European leveraged finance sprang back to life in 2024, as falling interest rates and a growing investor appetite laid the foundation for a return to a healthier market.

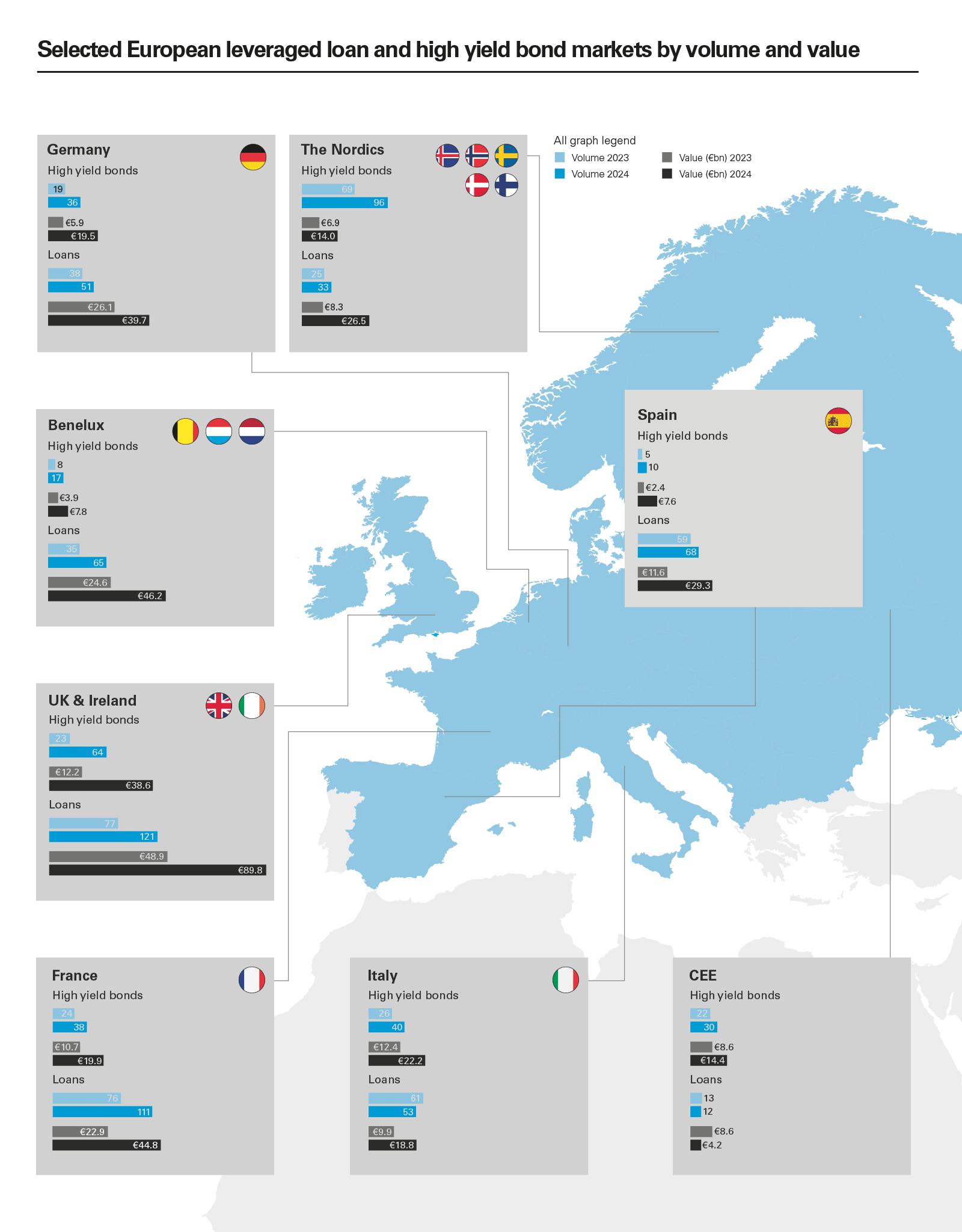

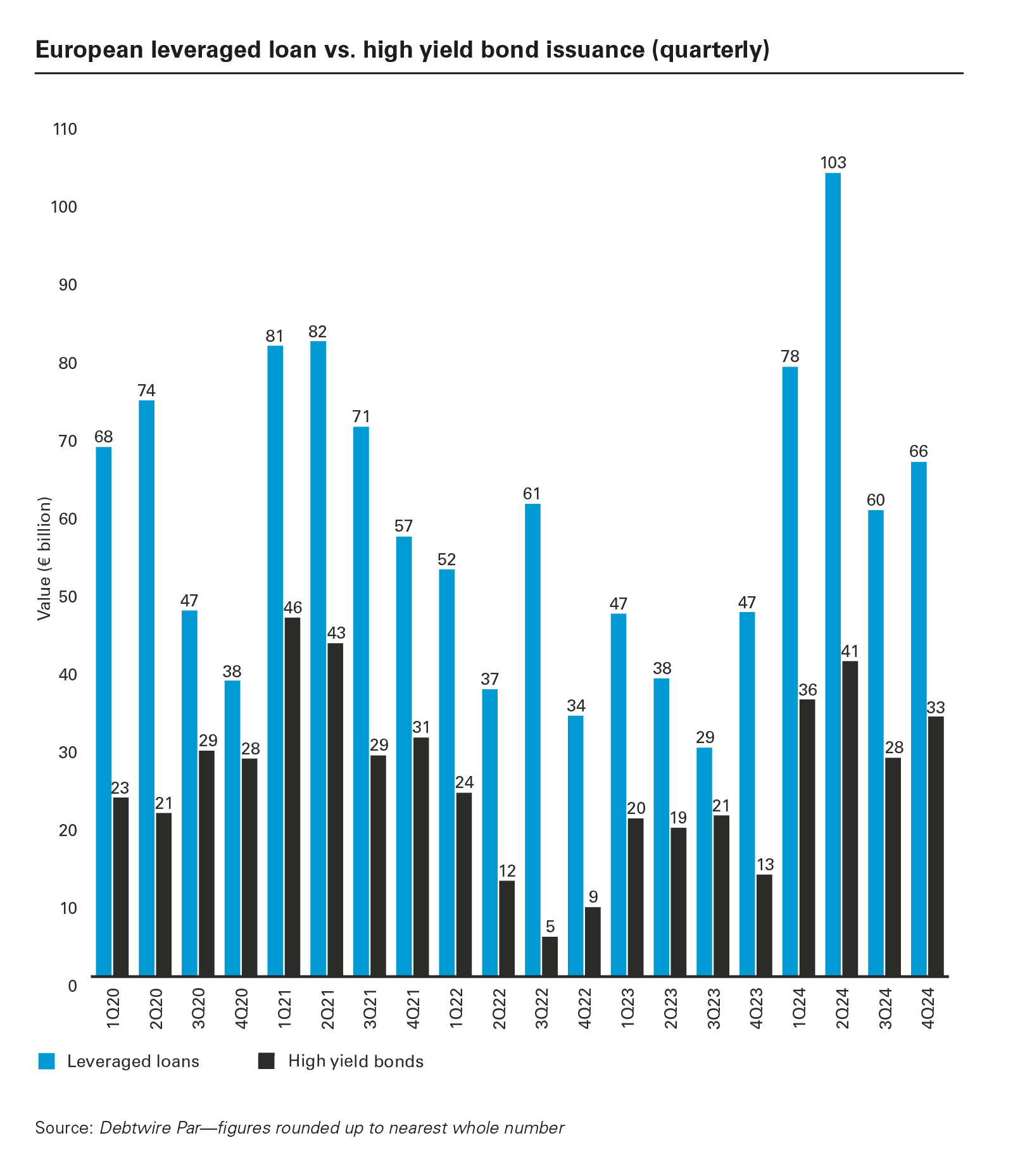

The aggregate value of leveraged loan issuance in Europe in 2024 (€307.4 billion) was almost double the annual total recorded in 2023 (€161.1 billion), with Q2 2024 generating the highest single-quarter total on record (€103.2 billion).

Europe's high yield bond markets were equally lively—indeed, issuance in H1 alone (€76.1 billion) surpassed the full-year sum recorded in 2023 (€73.2 billion), before rounding out to €137.6 billion for 2024 as a whole.

Falling interest rates have been the primary catalyst for the market's revival, with both the European Central Bank and Bank of England making interest rate cuts in 2024 for the first time in two and two-and-a-half years, respectively.

Lower rates have spurred activity in the collateralized loan obligation (CLO) space.

According to Debtwire, new euro CLO issuance was up 79.7 per cent year-on-year to €48.4 billion in 2024, as lower base rates pushed fixed-income investors to take on more risk to secure yield.

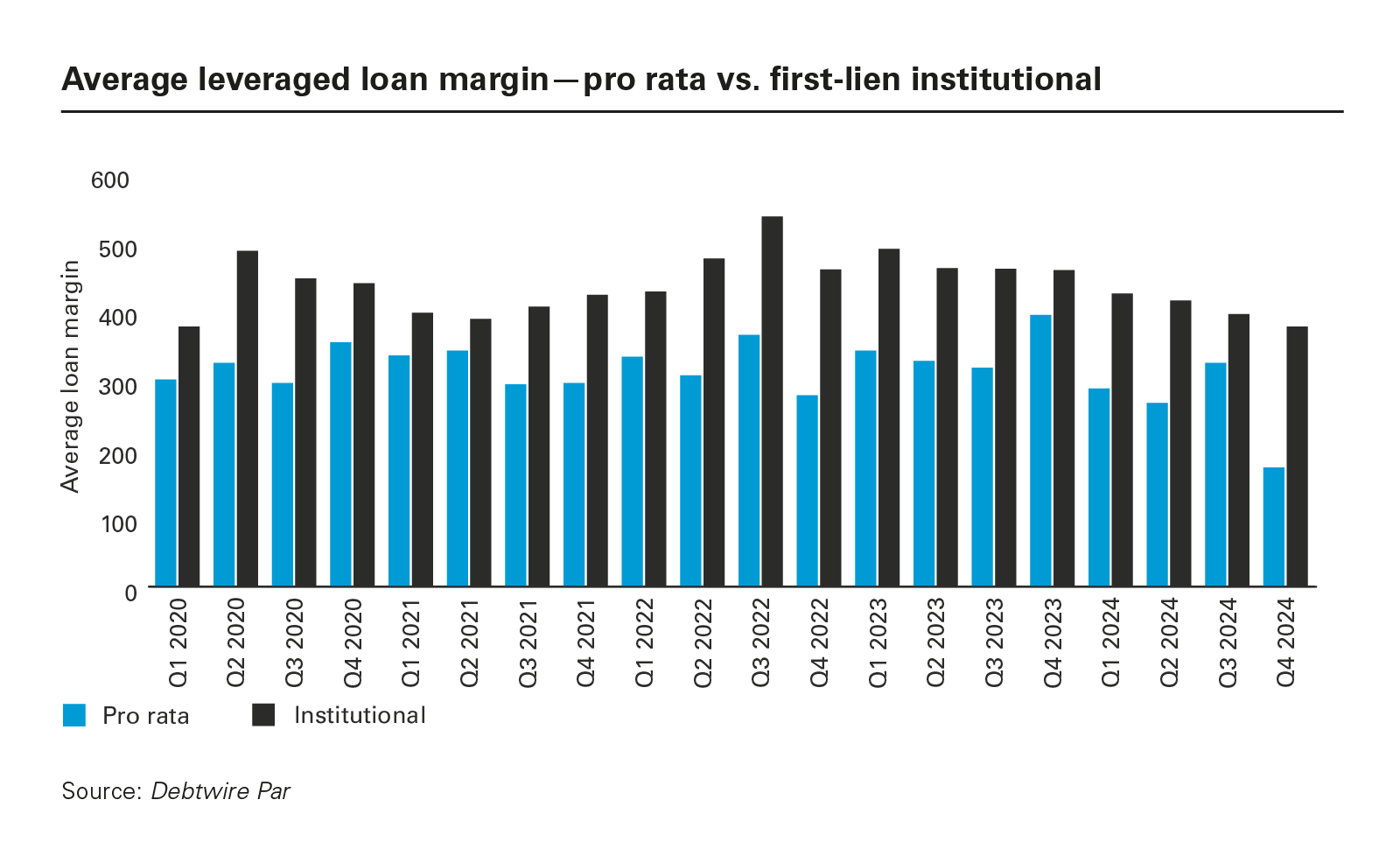

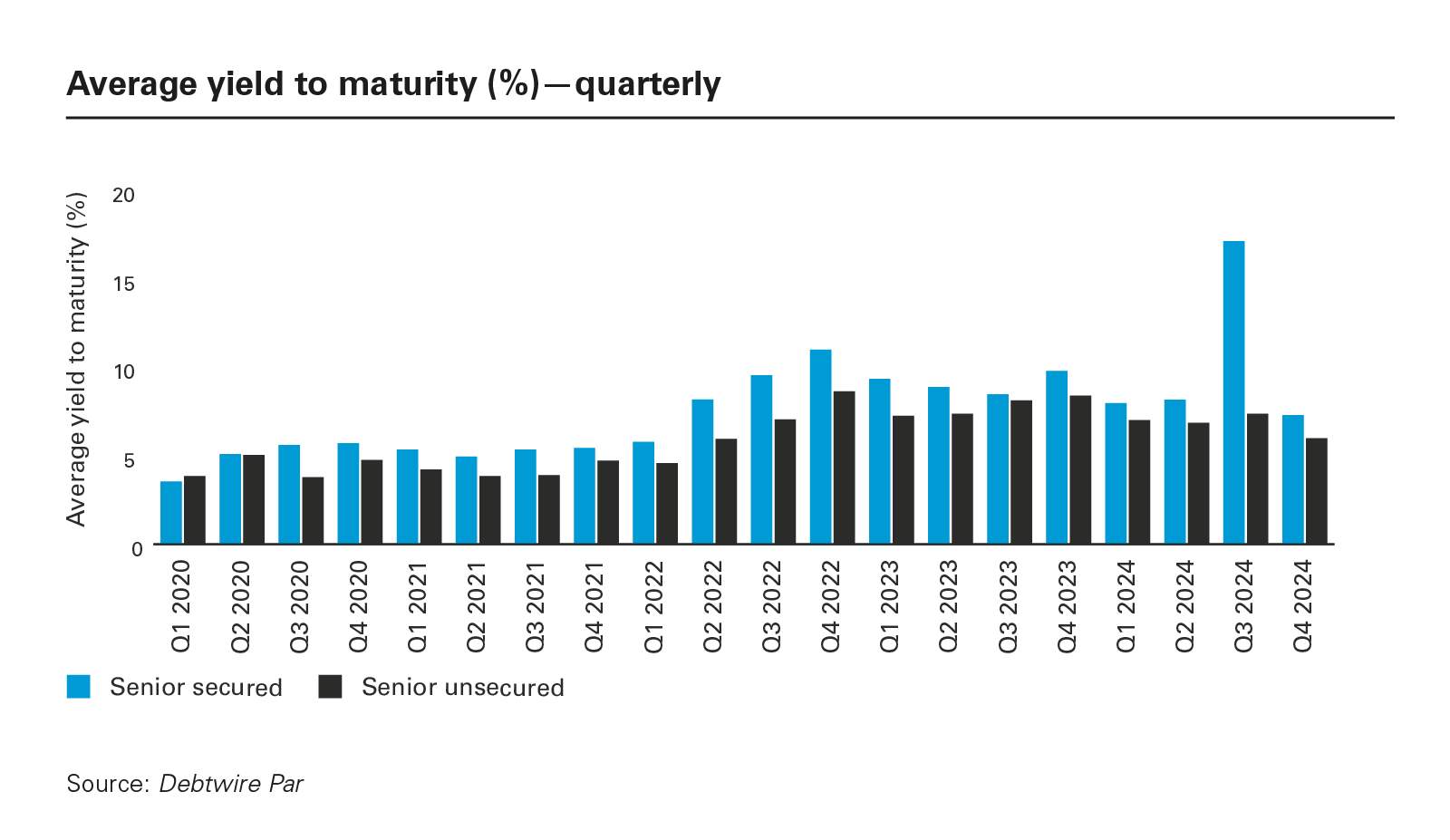

Lower base rates have also caused borrowing costs to fall, as have tighter margins in the leveraged loan markets and lower yields to maturity in the high yield space. Borrowers have jumped at the opportunity to refinance existing capital structures at lower prices.

In loan markets, refinancing issuance in 2024 was up 46 per cent year-on-year, reaching €161 billion and accounting for more than half of the overall issuance. In the high yield market, refinancing climbed to €85.1 billion, more than doubling last year's output, and generated almost two-thirds of the overall issuance in 2024.

The only piece of the puzzle missing from the market in 2024 was a full recovery in M&A and buyout transaction volumes.

Lower pricing in the broadly syndicated loan (BSL) and high yield markets has tipped the balance between public and private debt back in favour of public debt markets. Credits financed with more expensive private debt unitranche structures in some cases flipped back to BSL and high yield options over the course of 2024, as borrowers capitalised on lower costs during the year.

Phenna Group, backed by Oakley Capital, and Deutsche Fachpflege, a portfolio company of Advent International, are among the borrowers that have taken out private credit facilities with cheaper BSL borrowings. In early 2024, Neopharmed Gentili issued a €750 million senior-secured high yield bond to refinance a unitranche loan raised in 2022.

The increasing competition between BSL and private debt has directly benefitted borrowers. In addition to refinancing in the public debt markets, borrowers have been able to negotiate lower margins with incumbent private credit providers.

However, the dynamic between private debt and the BSL markets has not been an exclusively competitive one—some issuers are opting to include tranches of financing from both sources in their capital structures.

Some banks and private debt managers have formalised these relationships by establishing partnerships where banks leverage their branch networks and geographic footprints to originate loans. They can then be shared with private credit partners, so that banks do not have to hold the full loans on their own balance sheets. Citigroup and Apollo, and Lloyds Bank and Oaktree Capital Management, are among the lenders that have announced such partnerships.

A mature, sophisticated market

2024's wave of repricing and refinancing activity, in addition to the evolving relationship between public and private debt markets, is reflective of an increasingly sophisticated European loan market that is better able to respond quickly to changes in the business environment.

Investment banks, investors and borrowers were ready to spring into action as soon as interest rates began to recede, while remaining sensitive to any lingering concerns around risk. Few deals have priced outside of initial guidance, with all parties focused on seamless execution and completing deals with minimal disruption.

The only piece of the puzzle missing from the market in 2024 was a full recovery in M&A and buyout transaction volumes. But, if the speed of the market's response to an improving interest rate environment is anything to go by, chances are that lenders and borrowers will be ready to spring into action as soon as the first signs of a much-anticipated M&A revival materialise.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: European leveraged loan vs. high yield bond issuance (quarterly) (PDF)

View full image: Average leveraged loan margin—pro rata vs. first-lien institutional (PDF)

View full image: Average leveraged loan margin—pro rata vs. first-lien institutional (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)

View full image: Average yield to maturity (%)—quarterly (PDF)