After a challenging period of elevated rates, Europe's leveraged finance markets are poised for growth in 2025, with stabilising costs, rising competition and renewed opportunities for dealmakers.

European leveraged finance markets back on track

European leveraged finance markets rallied strongly in 2024, with momentum for new deals and opportunities for borrowers and lenders alike in 2025

Europe's leveraged finance markets enter 2025 following a solid performance in 2024, with the syndicated loan and high yield bond markets rallying and private debt remaining active. European loan and bond issuance nearly doubled year-on-year. Refinancing and repricing drove activity, as issuers returned to the market to take advantage of lower interest rates and bring down borrowing costs. With base rates falling, investors with a renewed appetite for yield have been eager to provide their support.

Moreover, with the revival of the loan and bond markets, borrowers have jumped at the opportunity to push out maturities and lower financing costs, and have in some cases taken the opportunity to refinance pricier unitranche structures provided by private debt players with cheaper loan and bond options.

This has created a fluid market where quality borrowers have had a broader range of products to choose from and the ability to select the best possible financing options to match their specific requirements.

Although public debt markets have regained market share, private debt players remain as relevant and active as ever, with their ability to price risk and deliver rapid deal execution.

With all the lending channels open again, the competitive dynamic between public and private debt providers has intensified to the benefit of the borrowers. Private debt players have tightened margins and offered more covenant flexibility to win new business. Public debt markets have sharpened execution and broadened the types of facilities they offer.

The only missing piece of the puzzle in 2024 has been a steady pipeline of new M&A and leveraged buyout financing opportunities.

This has been more of a function of an only moderately improving M&A deal market than a lack of investor and lender appetite. However, there is a growing optimism that deal activity will grow within the next 12 months, as interest rates come down and vendors and buyers align on valuation.

If and when the M&A market picks up, financing markets will be well positioned to support dealmakers.

European leveraged finance overview

Leveraged finance markets rallied in 2024 to record remarkable year-on-year gains

Interest rate cuts and tighter margins generated a surge in refinancing, as borrowers leapt at the chance to bring down financing costs

Bumper CLO issuance drove demand, with investors seeking yield as rates came down

A dynamic interplay between private debt and public debt continues to develop, with the two markets competing and, in some instances, collaborating

As rates fluctuate, private debt managers must adapt their investment strategies and risk management practices to navigate changing market conditions

Despite increased competition, private debt's ability to provide flexible solutions and focus on deep borrower relationships, and its active portfolio management, still set it apart from traditional lending

As the industry matures, strategic alliances between banks and private debt funds are slowly emerging to expand market reach

Old dog, new tricks: The evolution of syndicated loan markets

Insight

|

6 min read

Headlines

Broadly syndicated loan (BSL) markets have bounced back following a slowdown, regaining market share from private debt

Lower pricing has drawn sponsor-backed borrowers back to BSL financing options

Arrangers have kept a close eye on pricing, limiting the risk of flex and improving execution

BSL markets are increasingly offering flexible financing packages, including delayed draw optionality

With BSL markets in better health, we have seen some borrowers actively looking at the opportunity to refinance private debt facilities—which they had arranged when interest rates were climbing—with materially cheaper syndicated loans.

After a lengthy hiatus between H2 2022 and the end of 2023, BSL markets are back and hungry to finance deals. In 2024, European syndicated loan issuance nearly doubled the full-year figures the market recorded in 2023, driven by interest rate cuts in Europe and the UK, and tightening margins. This brought down financing costs for many borrowers, spurring a wave of refinancing activity.

Pricing play

Lower financing costs have enabled arranging banks to become more assertive when competing for business with direct lenders. The latter were able to win market share during the initial period of interest rate disruption in 2022, when syndicated loan markets activity had cooled.

With BSL markets in better health, we have seen some borrowers actively looking at the opportunity to refinance private debt facilities—which they had arranged when interest rates were climbing—with materially cheaper syndicated loans.

According to the S&P, approximately €10.5 billion of private debt in Europe was refinanced in the BSL and high yield bond markets during the first nine months of 2024, with companies securing median reductions to interest costs between 138 and 150 basis points.

Lower financing costs have also boosted the role of BSLs in leveraged buyouts (LBOs). The ratio of private debt-financed European LBOs to syndicated loan-financed LBOs narrowed from 10.5:1 in Q4 2023 to just 1.5:1 in Q2 2024, according to Deloitte.

BSL comes back better

While pricing has undoubtedly played a key role in the comeback of BSLs, other factors have also contributed to the syndicated loan market's competitive edge.

BSL arrangers, underwriters and investors have emerged from the cycle of rising interest rates sharper, stronger and better attuned to borrower and market requirements.

Investment banks have focused relentlessly on deal execution when underwriting and syndicating deals to avoid the risk of failed syndications and pricing flex. Indeed, Debtwire records show that no European leveraged loan deals experienced upward pricing flexes in either Q2 2024 or Q3 2024, following six consecutive quarters that all saw upward pricing flex between Q4 2022 and Q1 2024. Moreover, reverse flexes remained prevalent throughout 2024, with ten deals recorded in Q4 with an average cut of 25 basis points, demonstrating sustained market positivity as the year drew to a close. The improved visibility and certainty for pricing a BSL deal has aligned syndicated loans more closely with private debt, which has traditionally held an edge over the BSL markets in these areas.

New tricks

The BSL market has also become more flexible, with many stakeholders now offering features such as delayed-draw facilities in BSL loan packages.

This marks a significant evolution of the BSL product, with ratings agency Moody's noting that the shift in the terms offered is eroding the traditional distinctions between BSL deals and private debt.

The use of the delayed draw offer within the BSL structure illustrates how far the market has come to make its proposition more competitive. A delayed draw facility is a committed, unfunded term loan B debt facility that allows a borrower to draw down over an extended availability period rather than borrowing the entire amount at once. This appeals to borrowers, as they do not have to pay interest on debt that they are not using but have the comfort that (in exchange for a ticking fee or commitment fee) financing is available as soon as it is needed to fund capital expenditure or acquisitions. In some circumstances, this can be preferable to having to raise an additional or incremental facility on short notice. There are, however, some nuances that have arisen in the deployment of this type of facility in BSLs.

Although delayed draw has long been a feature of the private debt market, it has been more challenging to adapt to the BSL space. Syndicated loan investors prefer to put money to work immediately rather than commit to facilities that may only be drawn down later, if at all. As a result, selling committed but unfunded debt posed a challenge for banks that steered away from these structures due to the complexities of syndicating delayed draw debt.

To make the product more palatable to investors, banks have adapted delayed draw terms. Availability periods can be capped at 12 or 24 months, while ticking fee structures (where fees on the delayed draw facility, expressed as a percentage of the applicable margin, increase the longer a borrower waits to use it) reward investors if borrowers wait for a prolonged period before tapping into the facility. This is distinguishable from the private debt variant of delayed draw facilities where the commitment fee construct is typically more borrower-friendly and accrues at a (static) agreed percentage of the margin applicable to the delayed draw facility.

These adjustments mitigate the risk for investors of losing yield on undrawn facilities, and provide borrowers with confidence as they have access to long-term committed financing if required (albeit at a price). The value of this flexibility has been especially evident during the recent disruption in loan markets. Issuers have appreciated the security that a committed but unfunded facility offers, as it provides certainty when markets may be closed at the time of a bolt-on acquisition or major capital expenditure.

A more dynamic market

The way that BSL markets interface with private debt has also become more dynamic, as have the pathways to loan syndication. While BSL and private debt markets do compete with each other, syndicated markets have recognised the value of partnering with private debt players in certain circumstances.

For example, private debt providers can help enhance a capital structure by providing second-lien debt behind the first-lien financing raised in the BSL market. Meanwhile, the delta between the sterling and euro overnight lending rates has seen some private debt players fund the sterling-denominated portion of a loan, with the BSL market funding the euro-denominated portion.

Regarding the various routes to a syndicated loan, a select group of large-cap sponsors with the necessary scale and consistent deal flow have fleshed out their own syndication desks. These sponsors have found success in structuring and syndicating loan packages for their own deals directly, further enhancing the BSL market's functionality.

Despite facing challenges in recent years, the BSL market has demonstrated its ability to improvise, adapt and remain relevant, and enters 2025 stronger than ever.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

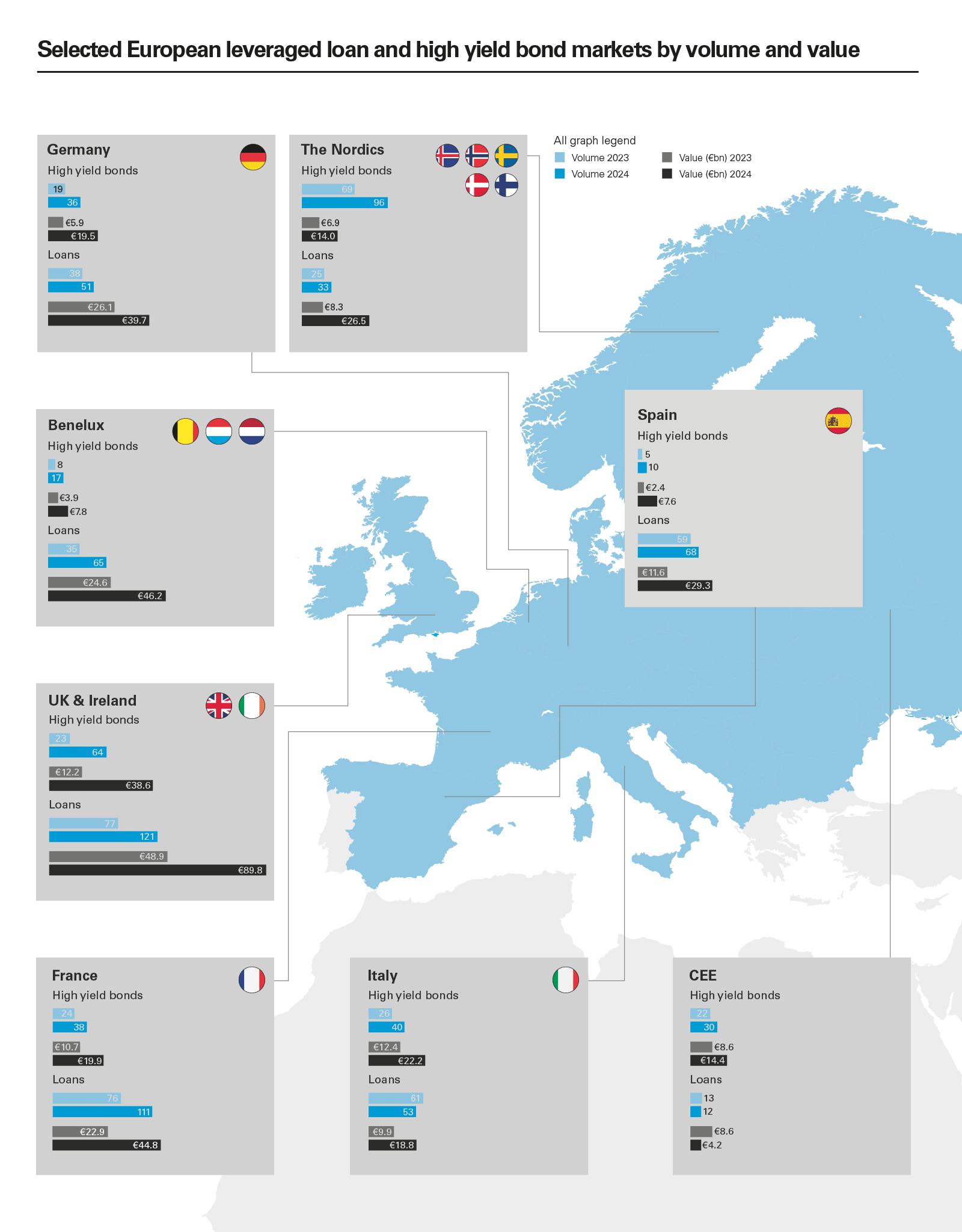

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)