After a challenging period of elevated rates, Europe's leveraged finance markets are poised for growth in 2025, with stabilising costs, rising competition and renewed opportunities for dealmakers.

European leveraged finance markets back on track

European leveraged finance markets rallied strongly in 2024, with momentum for new deals and opportunities for borrowers and lenders alike in 2025

Europe's leveraged finance markets enter 2025 following a solid performance in 2024, with the syndicated loan and high yield bond markets rallying and private debt remaining active. European loan and bond issuance nearly doubled year-on-year. Refinancing and repricing drove activity, as issuers returned to the market to take advantage of lower interest rates and bring down borrowing costs. With base rates falling, investors with a renewed appetite for yield have been eager to provide their support.

Moreover, with the revival of the loan and bond markets, borrowers have jumped at the opportunity to push out maturities and lower financing costs, and have in some cases taken the opportunity to refinance pricier unitranche structures provided by private debt players with cheaper loan and bond options.

This has created a fluid market where quality borrowers have had a broader range of products to choose from and the ability to select the best possible financing options to match their specific requirements.

Although public debt markets have regained market share, private debt players remain as relevant and active as ever, with their ability to price risk and deliver rapid deal execution.

With all the lending channels open again, the competitive dynamic between public and private debt providers has intensified to the benefit of the borrowers. Private debt players have tightened margins and offered more covenant flexibility to win new business. Public debt markets have sharpened execution and broadened the types of facilities they offer.

The only missing piece of the puzzle in 2024 has been a steady pipeline of new M&A and leveraged buyout financing opportunities.

This has been more of a function of an only moderately improving M&A deal market than a lack of investor and lender appetite. However, there is a growing optimism that deal activity will grow within the next 12 months, as interest rates come down and vendors and buyers align on valuation.

If and when the M&A market picks up, financing markets will be well positioned to support dealmakers.

European leveraged finance overview

Leveraged finance markets rallied in 2024 to record remarkable year-on-year gains

Interest rate cuts and tighter margins generated a surge in refinancing, as borrowers leapt at the chance to bring down financing costs

Bumper CLO issuance drove demand, with investors seeking yield as rates came down

A dynamic interplay between private debt and public debt continues to develop, with the two markets competing and, in some instances, collaborating

As rates fluctuate, private debt managers must adapt their investment strategies and risk management practices to navigate changing market conditions

Despite increased competition, private debt's ability to provide flexible solutions and focus on deep borrower relationships, and its active portfolio management, still set it apart from traditional lending

As the industry matures, strategic alliances between banks and private debt funds are slowly emerging to expand market reach

As rates fluctuate, private debt managers must adapt their investment strategies and risk management practices to navigate changing market conditions

Despite increased competition, private debt's ability to provide flexible solutions and focus on deep borrower relationships, and its active portfolio management, still set it apart from traditional lending

As the industry matures, strategic alliances between banks and private debt funds are slowly emerging to expand market reach

Rates are coming down slowly and in small increments. Throughout these fluctuations, private debt has continued to attract significant capital inflows and reinforce its position as a reliable alternative form of financing

Over the past few years, private debt has benefitted from higher interest rates that boosted the asset class's returns and default levels that remained in the low-to-mid single digits. Limited activity in the broadly syndicated loan (BSL) market allowed private debt managers to handpick the highest-quality credits for their portfolios.

However, market dynamics have recently evolved, reflecting a more competitive environment—base rates are falling and BSL markets have reopened. Competition for deals has intensified, and returns have decreased slightly as margins narrow and rate conditions loosen.

In this Q&A primer, White & Case provides an in-depth analysis of what lower interest rates and increased competition mean for private debt in 2025.

The European Central Bank and Bank of England both cut base rates for the first time in almost two years in 2024. What do lower rates mean for private debt?

Although base rates have declined, private debt's ability to provide tailored solutions has ensured it remains a cornerstone of financing strategies.

Moreover, Europe's rate hikes in 2022 and 2023, though notable, were not historically significant. At their peak, base rates were still moderate by long-term standards, and central banks issued clear forward guidance that rates would be elevated for only a short period of time. Now, rates are coming down slowly and in small increments. Throughout these fluctuations, private debt has continued to attract significant capital inflows and reinforce its position as a reliable alternative form of financing.

Will private debt have to accept lower returns given the lower base rates?

When speaking about returns, it is important to focus on risk-adjusted performance rather than absolute figures. When rates are elevated, lenders can tell investors that total returns have increased, but this is typically offset by the rising risk-free rate. The spread over the risk-free benchmark, as a measure of relative performance, remains stable in those circumstances.

In a mature, liquid and competitive market, the risk-adjusted return across all assets tends to converge over the long term. In the early days of private debt, the risk-adjusted return was at a premium compared to other asset classes. But now, with the market becoming significantly more competitive, that premium is no longer available. Instead, investors today are attracted to private debt because the asset class presents less risk than, for example, public equities but continues to offer a premium over treasuries and bonds.

How has the competitive landscape shifted during the past 12 months?

Following a four-to-five-month hiatus, the reopening of the BSL market has introduced new dynamics, which has required private debt managers to adapt and become even more innovative. In early 2024, several private debt deals were being repriced into the syndicated market, prompting private managers to respond. Unitranche pricing has adjusted and margins have narrowed slightly, from five-and-a-half or five-and-three-quarter points above the base rate to approximately five percentage points over. Moreover, several private debt managers have been offering borrowers the option to extend non-call periods in exchange for a margin reduction, which lowers the coupon for the private debt provider but secures a longer-term lender position.

Of course, private debt managers can only afford to lower margins to a certain extent, but they are focusing more intensely on financing deals where their expertise and flexibility create the most value. For instance, a large-cap sponsor that is looking to acquire a European business with a strong credit profile using an entirely euro-denominated debt package is likely to raise a loan or a bond to finance the acquisition.

But for deals involving more complex credit profiles—such as those that require a large quantum of sterling-denominated debt, a large-delayed draw facility or payment-in-kind (PIK) flexibility—private debt is especially well positioned. Depending on the loan requirement, and as long as the pricing between the BSL offerings and private debt is not intolerably wide, there are still numerous reasons for sponsors to go private.

Defaults have increased, but only marginally. Has this come as a surprise given the elevated interest rates?

The rise in defaults has been modest and broadly in line with long-term averages. Although base rates have increased by around a factor of ten, they remain well below their historical high points. Given the sufficient forward guidance from policymakers and with careful planning, strong credits have been more than able to weather these conditions.

Moreover, the private debt community benefits greatly from its ability to grant PIK flexibility and waive cash coupons in circumstances where managers are convinced of the borrower's long-term business prospects. This flexibility and the absence of covenants, especially in larger deals, helps to ease the pressure on borrowers.

Private debt managers pride themselves on understanding the businesses they finance, poring over monthly and quarterly reports, engaging with sponsors and holding regular management meetings to obtain a comprehensive understanding of the business. This attention to detail enables private debt managers to respond swiftly and effectively to sponsors' requests, provided that sponsors continue to provide the detailed reporting that lenders expect.

In comparison to BSL managers, private debt managers typically oversee smaller portfolios comprising fewer, better-understood loans that they proactively manage. When borrowers encounter challenges, an informed private debt manager is on call to make quick decisions and offer support. By contrast, syndicated deals can be significantly more cumbersome given the large number of different lenders that are typically involved.

What are we to make of partnerships between banks and private debt funds? How do the parties benefit from this?

This trend is beginning to emerge. In theory, these partnerships present interesting possibilities. Large banks leverage their existing branch networks and broader geographical coverage to structure deals without committing large sums of their own capital.

For the private debt managers, who usually do not have a large footprint across multiple jurisdictions, these partnerships facilitate enhanced deal origination. And among the borrowers, these partnerships can improve execution timelines, while also reducing syndication and flex risk. How this evolves in practice over the coming year will need to be closely observed.

Looking ahead to 2025, what will private debt managers be prioritising?

Private debt players will focus on their core competencies. Specifically, rapid decision-making, competitive pricing and their deep relationships with borrowers. Those qualities will be especially important if the much-anticipated revival of the M&A and leveraged buyout markets materialises in 2025.

Overall, private debt managers are well positioned to capitalise on the forecasted uptick in dealmaking, underlining their relevance in the evolving financial landscape.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

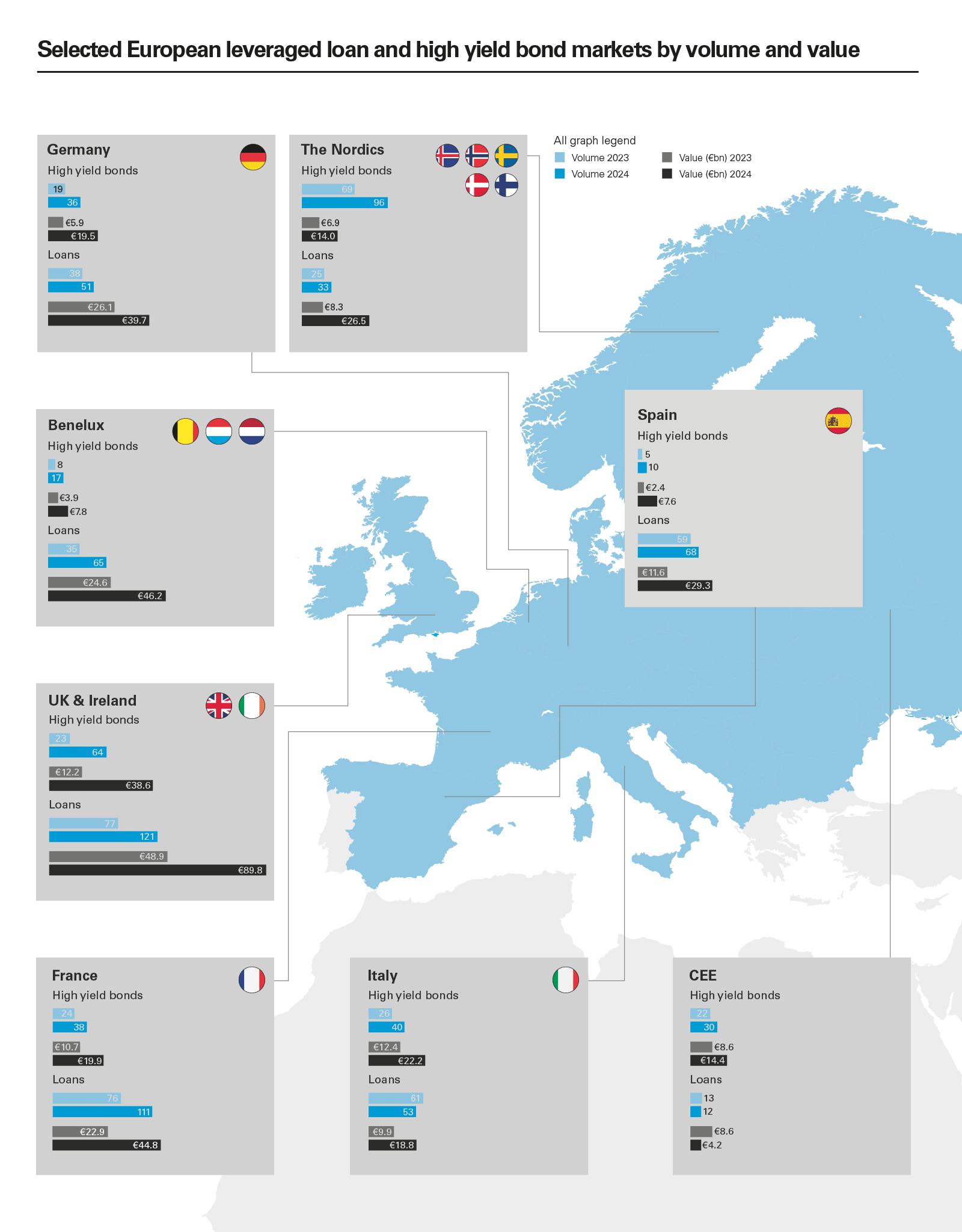

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)