After a challenging period of elevated rates, Europe's leveraged finance markets are poised for growth in 2025, with stabilising costs, rising competition and renewed opportunities for dealmakers.

European leveraged finance markets back on track

European leveraged finance markets rallied strongly in 2024, with momentum for new deals and opportunities for borrowers and lenders alike in 2025

Europe's leveraged finance markets enter 2025 following a solid performance in 2024, with the syndicated loan and high yield bond markets rallying and private debt remaining active. European loan and bond issuance nearly doubled year-on-year. Refinancing and repricing drove activity, as issuers returned to the market to take advantage of lower interest rates and bring down borrowing costs. With base rates falling, investors with a renewed appetite for yield have been eager to provide their support.

Moreover, with the revival of the loan and bond markets, borrowers have jumped at the opportunity to push out maturities and lower financing costs, and have in some cases taken the opportunity to refinance pricier unitranche structures provided by private debt players with cheaper loan and bond options.

This has created a fluid market where quality borrowers have had a broader range of products to choose from and the ability to select the best possible financing options to match their specific requirements.

Although public debt markets have regained market share, private debt players remain as relevant and active as ever, with their ability to price risk and deliver rapid deal execution.

With all the lending channels open again, the competitive dynamic between public and private debt providers has intensified to the benefit of the borrowers. Private debt players have tightened margins and offered more covenant flexibility to win new business. Public debt markets have sharpened execution and broadened the types of facilities they offer.

The only missing piece of the puzzle in 2024 has been a steady pipeline of new M&A and leveraged buyout financing opportunities.

This has been more of a function of an only moderately improving M&A deal market than a lack of investor and lender appetite. However, there is a growing optimism that deal activity will grow within the next 12 months, as interest rates come down and vendors and buyers align on valuation.

If and when the M&A market picks up, financing markets will be well positioned to support dealmakers.

European leveraged finance overview

Leveraged finance markets rallied in 2024 to record remarkable year-on-year gains

Interest rate cuts and tighter margins generated a surge in refinancing, as borrowers leapt at the chance to bring down financing costs

Bumper CLO issuance drove demand, with investors seeking yield as rates came down

A dynamic interplay between private debt and public debt continues to develop, with the two markets competing and, in some instances, collaborating

As rates fluctuate, private debt managers must adapt their investment strategies and risk management practices to navigate changing market conditions

Despite increased competition, private debt's ability to provide flexible solutions and focus on deep borrower relationships, and its active portfolio management, still set it apart from traditional lending

As the industry matures, strategic alliances between banks and private debt funds are slowly emerging to expand market reach

Five key stakeholders and their priorities in 2025

Insight

|

5 min read

Headlines

Investment banks will leverage their networks and multidisciplinary expertise to execute deals

Private debt players will remain nimble to offer solutions in a dynamic market

Borrowers will stay prepared to move quickly to capitalise on increasingly supportive conditions in financing markets

Private equity sponsors will see a mix of providers of financing for new deals

Emergent US-style liability management transactions will reshape the way European credit managers operate

Expect investment banks to adopt more dual-track processes and craft bespoke debt packages that combine traditional public capital markets with private debt and other alternative financing providers.

European leveraged finance markets enter 2025 on firmer footing than a year ago, and will present borrowers and lenders with a dynamic mix of opportunities and risks. Below, White & Case reflects on how five key stakeholder groups will approach leveraged finance this year.

Investment banks

Investment banks played a fundamental role in the reopening of the leveraged finance markets in 2024 after two years of reduced activity, and will continue to prioritise deal execution and syndication stability in the year ahead.

Keeping a close watch on the changing market dynamics and aligning terms and pricing strategies will be crucial to minimising pricing flex and avoiding failed syndications. Rather than pushing investors to their limit, banks will focus on identifying pressure points and adopting pragmatic approaches to close deals for their clients.

Bankers will endeavour to maintain stability in the face of geopolitical uncertainty, global conflicts and escalating trade tensions by leveraging their networks and multidisciplinary teams. Expect investment banks to adopt more dual-track processes and craft bespoke debt packages that combine traditional public capital markets with private debt and other alternative financing providers. Sizable back-office teams and robust information flows will enable banks to provide precise guidance amid challenging market conditions.

Private credit funds

Private debt funds will face stiff competition from re-energised broadly syndicated loan (BSL) markets for large-scale financings in 2025. To remain competitive, they will again emphasise their core strengths, offering flexible and bespoke financing solutions.

In response to certain borrowers refinancing in the BSL markets to secure better pricing, private debt players in 2025 may look to retain borrowers by offering margin reductions.

However, private debt will not be entirely on the defensive in 2025. It will remain the primary source of financing for mid-market buyouts, and the preferred option in large, intricate deals that may be challenging for BSL markets to digest or fully cover due to elevated levels of leverage or higher perceived operational risk.

Private debt has demonstrated its ability to deliver financing for big-ticket transactions during the recent interest rate cycle. With their focus on comprehensive due diligence and tailored financing packages, private debt managers will be able to position themselves as the go-to solution for loans deemed too risky or complicated for BSL markets.

Borrowers

BSL markets are again open for business, while private debt players continue to offer a valuable alternative path to financing. For borrowers, 2025 will present many opportunities to procure attractive financing deals as various lenders compete for their business.

Borrowers have already taken advantage of the reopening of the BSL markets by securing lower prices. Refinancing and repricing activity in Europe recorded significant year-on-year gains in 2024. With further interest rate cuts forecast for 2025, borrowers will be in an enviable position to further reduce financing costs by optimising deal timing. Flexibility and preparation will be key to ensuring that all financing routes are available to borrowers and to allow them to pivot to new options if any one market experiences a slowdown.

Private equity sponsors

Private equity sponsors enter 2025 confident that debt markets will be able to deliver acquisition financing when deal opportunities arise. Sponsors will mix public and private debt sources to optimise capital structures. For instance, more deals may see banks and syndicated markets provide senior loans, while private debt players contribute payment-in-kind debt and preferred equity tranches.

The most important catalyst for increased sponsor activity will be the long-anticipated revival of M&A and buyout markets, with the gap between the buyer's and seller's price expectations beginning to narrow. The Argos Index, which tracks the multiples paid for European private M&A targets, recorded improving deal multiples in Q3 2024 after three years of decline.

These data points are indicative of a market primed for dealmaking, with financing markets ready to meet that demand.

Hedge funds

Although European non-investment-grade default rates remain elevated relative to historical levels, they have not exceeded five per cent, and credit trends remain broadly supportive. Sponsors and lenders have taken crucial steps to prevent defaults and avoid major debt restructurings, employing a variety of tools such as covenant waivers, equity cures, interest payment holidays and maturity extensions to disrupt the normal default cycle.

Perhaps the most important driver of this shift in 2025 will be the increasing prominence of US-style liability management deals in Europe. These deals, which involve strategic restructurings of debt hierarchies—with opportunistic lenders moving to the top of the capital structures by ‘up-tiering,' or carving out certain assets from company balance sheets to serve as security for new money—have been commonplace in the US, but remained quite novel on this side of the Atlantic.

However, in 2024, the first few high-profile liability management deals were executed in Europe. Although potentially controversial, and notwithstanding the 31 December 2024 New York court decisions with respect to Serta and Mitel, it is likely that this trend will continue to grow, which may be a boon for opportunistic credit investors.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

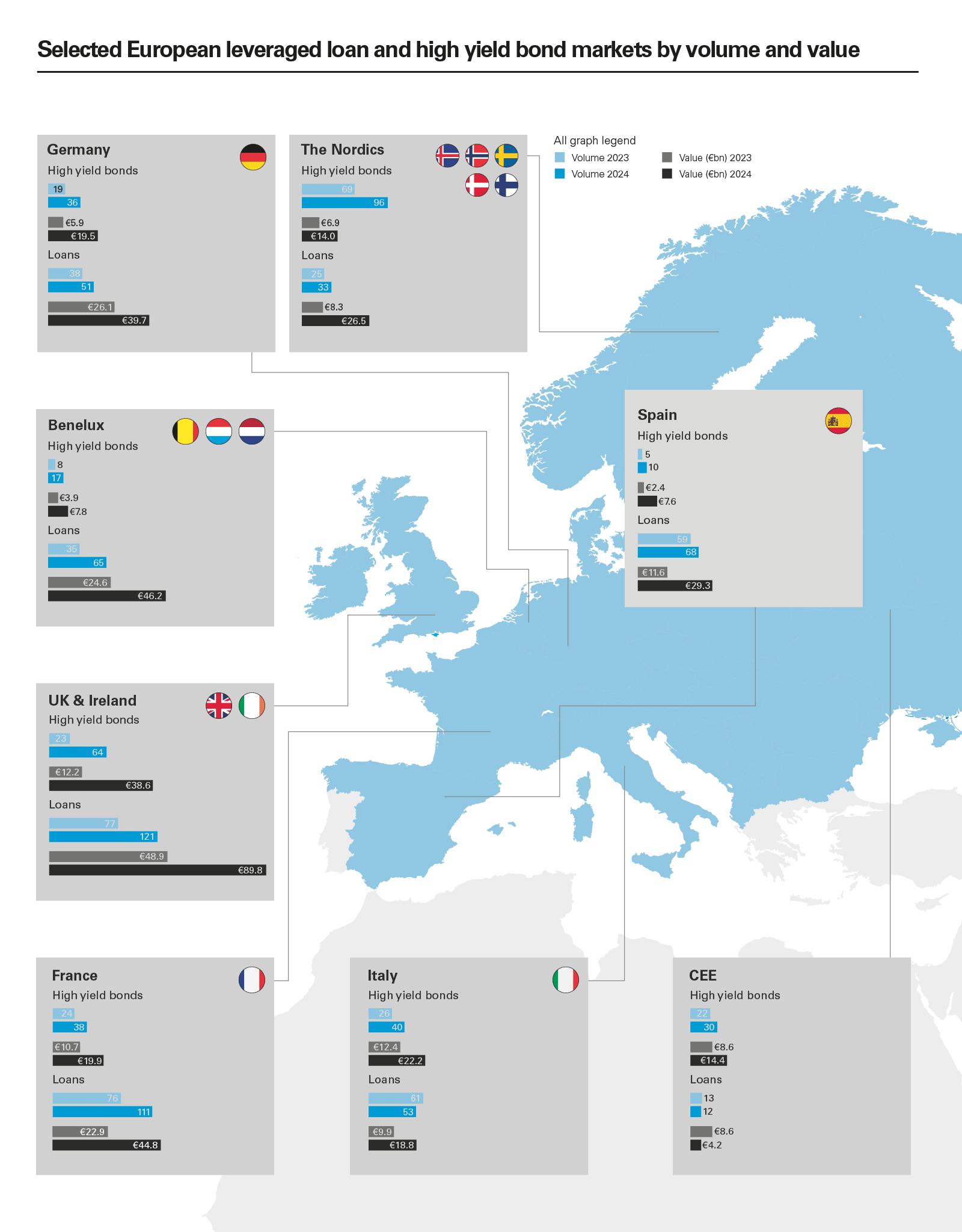

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)