Headlines

- Despite volatile political conditions and weak GDP growth, debt markets in Germany and France outperformed expectations in 2024

- Falling interest rates drove a surge in loan issuance in both countries

- Private credit firms continue to underwrite landmark unitranche financings

- Borrowers and sponsors are collaborating on hybrid structures to optimise pricing and terms

Despite political uncertainty and fragile GDP growth, debt markets in continental Europe's two largest economies—France and Germany—made strong gains in 2024.

A hung parliament in France following snap elections in the summer left the country unable to pass a budget, while Germany will hold new elections in 2025 after its incumbent coalition fractured in November. This political uncertainty has been compounded by weak economic growth forecasts. Both the French and German economies are expected to expand by less than one per cent in 2025, according to OECD forecasts.

Rate cut relief

Amid the macroeconomic turmoil, capital markets in both France and Germany outperformed expectations in 2024. A series of four interest rate cuts by the European Central Bank throughout the year—with base rates falling from a record four per cent in June to three per cent in mid-December—gave markets enough momentum to persevere.

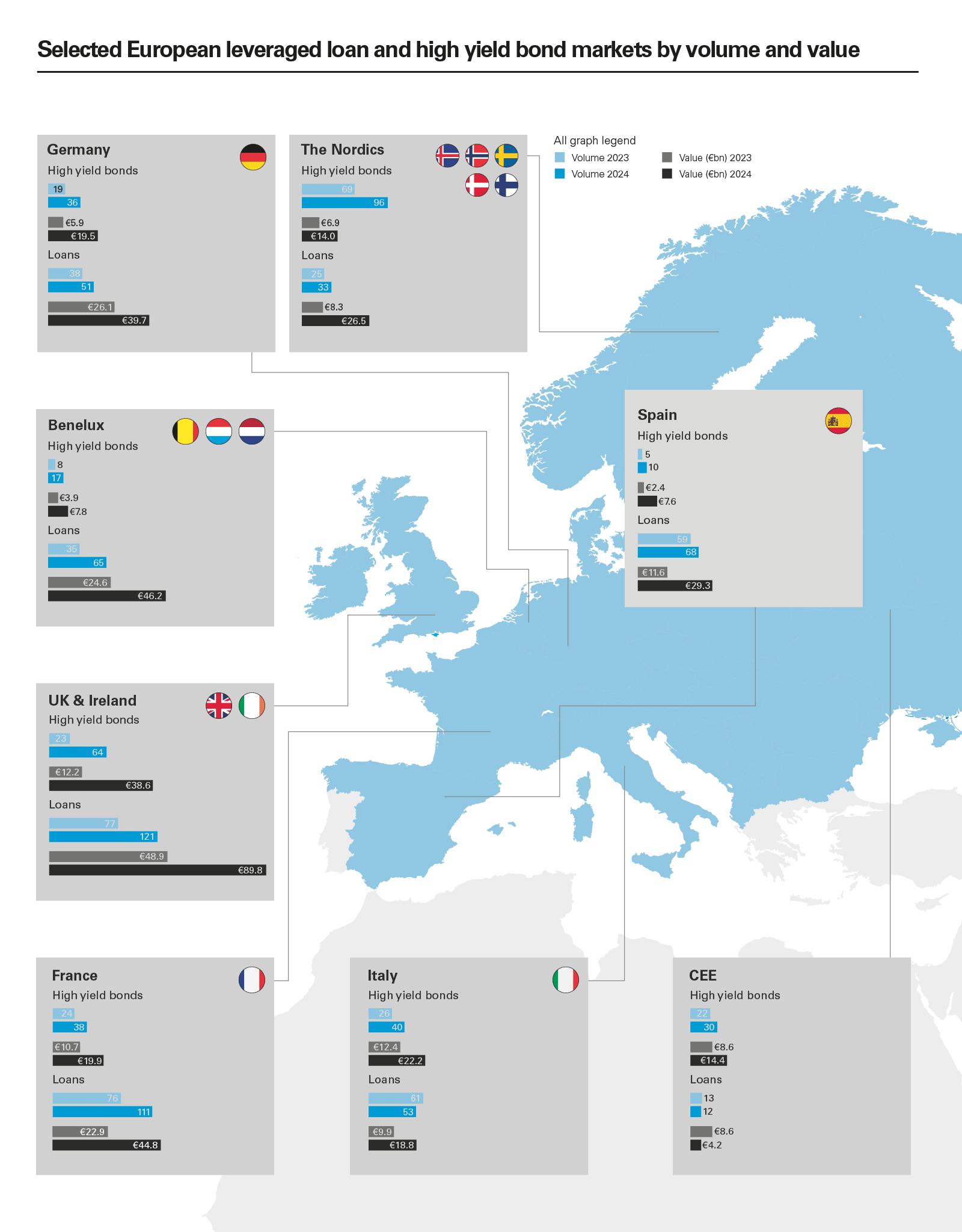

Syndicated leveraged loan issuance in Germany rose by 52.2 per cent year-on-year in 2024, climbing from €26.1 billion in 2023 to €39.7 billion. Meanwhile in France, leveraged loan issuance almost doubled year-on-year, reaching €44.8 billion in 2024.

High yield markets in each country were equally robust. German high yield issuance reached €19.5 billion in 2024, more than three times the figure recorded the year prior (€5.9 billion). French high yield markets also performed very strongly, with issuance of €19.9 billion representing an 86 per cent increase over 2023's total of €10.7 billion.

Window for opportunity

Similar to other European countries, French and German issuance has been spurred by refinancing and repricing activity. As base rates were trimmed and margins tightened, issuers leapt at the opportunity to decrease their borrowing costs.

In Germany, refinancing issuance of €24.9 billion in 2024 accounted for more than three-fifths of the overall issuance. In France, refinancing came in at €21.2 billion last year, representing just under half of the overall issuance.

Lower rates and the reopening of broadly syndicated loan (BSL) markets have introduced a competitive impetus in both countries, where alternative financing options became more prominent during the cycle of climbing interest rates. As rates began to increase in 2022, private debt players gained considerable market share in France and Germany, as the BSL and bond markets became more constrained.

Bank club financings and Schuldscheine (privately placed debt instruments, often used by large corporates on an unsecured basis or for real estate financings on a secured basis) are additional alternative financing sources used by many borrowers in 2022, 2023 and at the start of 2024. Sparkassen, Germany's regional savings banks, expanded their buyout financing footprints during this period for small and mid-cap financings.

The revival of the bond and BSL markets in 2024 has squeezed private debt players, with clients choosing to refinance unitranche facilities through cheaper loan and bond markets.

Some borrowers have retained unitranche facilities but have leveraged favourable market conditions to negotiate lower coupons with private debt managers in exchange for extending non-call periods. French calibration and testing laboratory group Trescal and Paris-based pharmaceuticals group Unither are among the borrowers who have been able to reprice existing unitranche loans in this way.

Mix, match and maximise

Although alternative financers have faced more competition from public debt markets, they remain open for business. Germany's Sparkassen are still active in the acquisition finance space, clubbing together to provide customised packages for M&A transactions. Likewise, the investment-grade Schuldscheine market always retains liquidity for the right type of borrower, even during periods of economic volatility.

Large unitranche packages financed by direct lending have also continued. For example, German payments company SumUp landed one of the largest-ever European private credit deals in 2024 when it secured €1.5 billion from a group of lenders led by Goldman Sachs, while German property-management software company Aareon took on a €1.35 billion Blackstone Credit–led private debt financing. Overall, France and Germany are now firmly established as the second- and third-largest private debt markets in Europe, behind only the UK.

For borrowers, the reopening of all these various financing channels has presented a unique window of opportunity to mix and match different borrower groups and tailor the most attractive and flexible financing packages.

Many deals that would once have gone directly through the BSL or bond markets due to their pricing advantages are now running dual-track processes. This allows borrowers to compare offers from various providers and potentially incorporate different lenders in hybrid structures, capitalising on the pricing benefits of syndicated options and the flexibility of private credit.

Although geopolitical and macroeconomic conditions are likely to remain challenging for French and German companies in 2025, debt markets are expected to stay open for business, offering a diverse range of financing options to support borrowers.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)