Since the publication of our first report, "Navigating India: Lessons for Foreign Investors," in 2013, India has undergone a remarkable transformation. The country's population grew by 100 million. Fuelled by improved connectivity and digital infrastructure, the number of internet users has soared, with more than half of its citizens now connected to the internet— a significant increase from the mere 12 per cent recorded in 2013. India's GDP has more than doubled, rising from US$1.8 trillion in 2013 to US$3.9 trillion in 2024, underscoring the nation's robust growth trajectory. Per capita income has also improved, reaching US$2,700 in 2024 compared to US$1,400 in 2013.

The Indian government's ambitious programme of regulatory reforms, aimed at making the country an attractive option for international investors, is clearly bearing fruit. In the World Bank's 2020 "Ease of Doing Business" report, India rose to the 63rd position out of 190 countries, marking a significant improvement from its 134th place in 2013. In this compendium, we highlight business opportunities and discuss some of challenges India faces today.

One such challenge is the high-valuation multiples of Indian companies, which have historically dampened cross-border M&A. While these high-valuations present lucrative opportunities for businesses to monetise through listings, they also pose challenges in structuring deals, particularly those involving India-listed subsidiaries and combinations with non-Indian businesses. However, recent regulatory changes, such as permitting share swaps and foreign investors' growing acceptance of Indian securities, are paving the way for innovative deal structures.

India's commitment to achieving net-zero by 2070 is another key issue. The country is pressing ahead with legislative reforms and investment into energy transition on an unprecedented scale, with renewables at the heart of this drive. India has the potential to increase its renewable energy production vastly—whether in solar, wind, hydro, hydrogen or other forms of renewables—and it is making various incentives available to accelerate that process. Legislation and new schemes should make the country even more attractive to investors, and indeed the efforts are already paying off, with a significant number of large investments being committed in recent years.

Technology is also a growth sector. Several multibillion-dollar deals by companies such as Amazon and Apple emphasise the potential of the tech economy. Meanwhile, in infrastructure, the introduction of products such as infrastructure investment trusts and real estate investment trusts make investment by foreign companies more attractive

However successful an investment, there will come a time to exit. In this issue, we examine two ways of exiting Indian investments: through general partner-led secondary transactions and through the public market. Those wishing to exit must plan ahead and put the necessary protections into their documentation at an early stage to avoid potential pitfalls down the track.

India has also made significant strides in reforming its alternative dispute resolution framework, aiming to position itself as a global hub for international arbitration. The 2021 Mediation Bill is another progressive step in making commercial disputes easier to handle, and the supportive stance of Indian courts has amplified positive effects of the legislative reforms.

Investing in India has never been more attractive for foreign investors, and we hope you will find this issue an insightful read.

Indian cross-border investment riding high in booming debt finance market

Against a challenging macro-economic environment worldwide, India has proven resilient and demonstrated its huge potential for growth. With an increasingly favourable regulatory regime and greater avenues of investment, India’s attractiveness as a global market for investors will only continue.

India’s thriving IPO market bucks the global trend

India stands out globally as a market with strong growth in IPO volume, thanks to its dynamic regulatory framework, robust domestic capital market and a large retail investor base. IPOs are also gaining popularity among foreign investors as one of the available exit options from their investments.

Indian cross-border M&A: High valuation hurdles and the hopeful path ahead

Foreign investors in India have historically faced numerous challenges, from high-valuation multiples to regulatory limitations, but evolving market conditions are cause for hope.

The rise of single-asset GP-led secondaries in the Indian investment landscape

The market for private equity-led secondary transactions is growing, and India is steadily catching up with the global trend in embracing these innovative exit strategies.

India’s legal reform in dispute resolution encourages foreign investment

In the past decade, India has made significant strides in reforming its alternative dispute resolution (ADR) framework, aiming to position itself as a global hub for international arbitration. The supportive stance of Indian courts towards arbitration has amplified the positive effects of these reforms.

Indian cross-border M&A: High-valuation hurdles and the hopeful path ahead

Foreign investors in India have historically faced numerous challenges, from high-valuation multiples to regulatory limitations, but evolving market conditions are cause for hope.

In January 2024, India overtook Hong Kong as the world's fourth-largest stock market

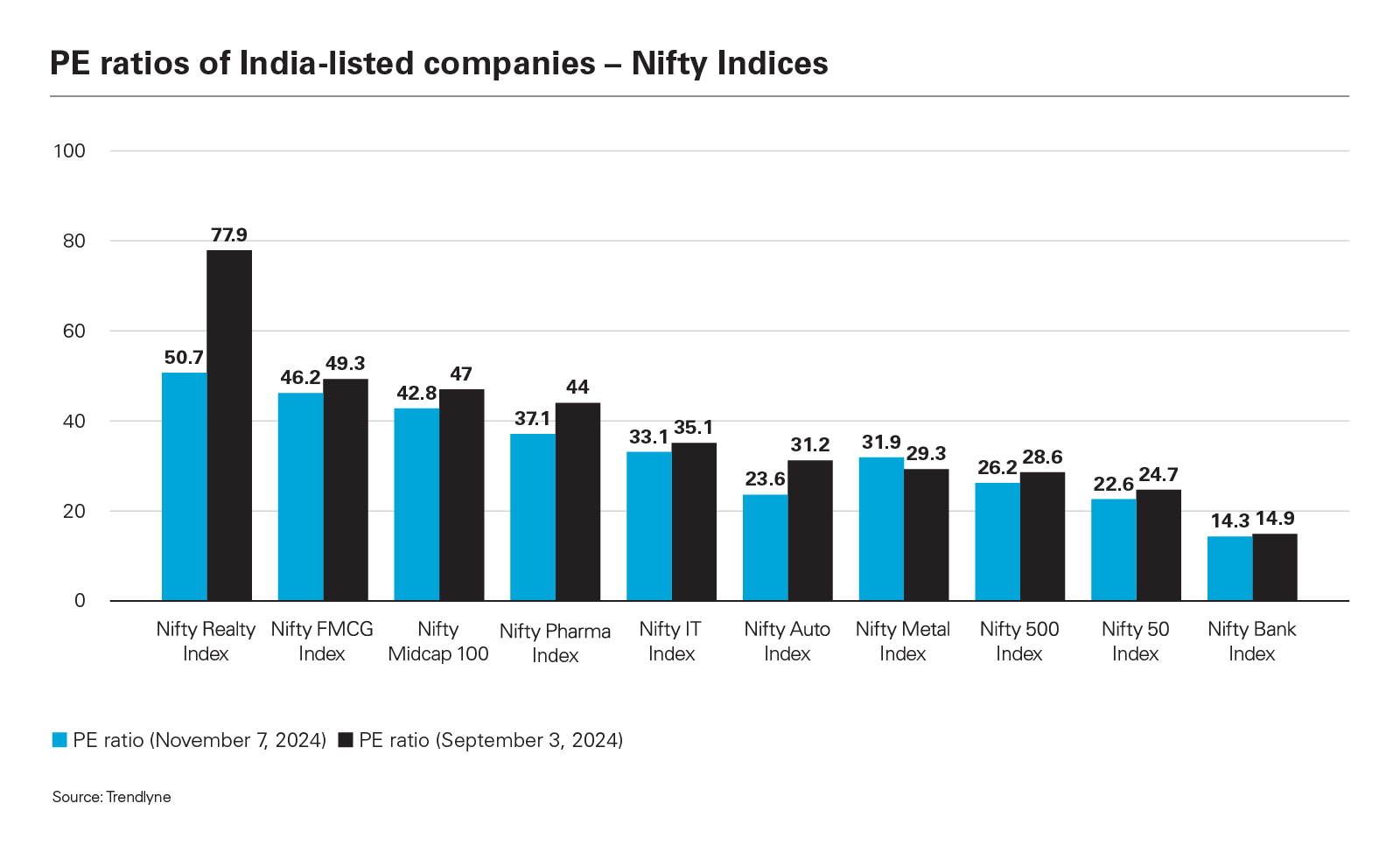

Indian companies have attracted significant attention for their high-valuation multiples, often surpassing those seen in other global markets for companies in the same sector. This has led to a surge in businesses seeking listings in India. The IPO deluge has included Indian subsidiaries of global businesses, venture capital-backed Indian startups such as FirstCry and Ola Electric, and private equity-backed businesses seeking exit for their financial sponsors, including Aadhar Housing Finance, Premier Energies and RR Kabel.

The listing of Indian subsidiaries such as Hyundai Motors India is a new phenomenon, since historically global businesses often made considerable efforts to take their subsidiaries private, as seen with Sandvik, Cadbury and Reckitt. At the time, these companies were forced to list in India due to a regulatory requirement that required foreign companies to divest stakes in their Indian subsidiaries to Indian shareholders. In many cases, Indian businesses that had set up or made considerable efforts to domicile their holding companies outside the country are now re-domiciling in India to benefit from the favourable market conditions.

However, this high-valuation trend has brought several unique challenges in the realm of M&A involving Indian companies, while also paving the way for innovative deal structures and regulatory changes that could enhance cross-border dealmaking.

The high-valuation multiples of Indian companies are a testament to the country’s robust economic growth, favourable demographics, digital transformation and supportive government policies. In late January 2024, India overtook Hong Kong to emerge as the fourth-largest stock market, based on market value. However, while these high-valuations offer lucrative opportunities for businesses to monetise through listings, they also pose significant challenges in the M&A landscape.

Challenges in cross-border M&A

Global deals for companies with India-listed subsidiaries: International deals involving companies with India-listed subsidiaries have faced hurdles due to the requirement for cash payouts to Indian public shareholders. These payouts are necessitated by regulations that aim to protect minority shareholders, but the subsidiaries’ high-valuation multiples and the requirement for payouts to be based on a subsidiary’s trading price often mean that payouts are at a much higher valuation than that of the subsidiary’s business in the global deal. This has sometimes made global companies with India-listed subsidiaries unattractive to potential buyers.

Combinations or mergers between Indian and non-Indian businesses: Transactions that bring together or combine India-listed companies and non-Indian companies to create global sector leaders have often been stymied by the need to pay cash to both controlling and public shareholders of India-listed companies. The high multiples at which Indian companies trade make these payouts substantial and the entire deal unviable. Even when controlling shareholders have been willing to accept a lower price, exchange control regulations have acted as a barrier, since they require transfers by residents to non-Indian buyers to be at least at the fair market value.

Monetising high multiples for acquisitions outside India: Indian companies have struggled to leverage their high-valuation multiples as acquisition currency in international markets. The disparity in valuation expectations and regulatory hurdles—where it was unclear for a long time whether share swaps required regulatory approval and, if so, whether such regulatory approvals would be easily forthcoming—have limited Indian companies’ ability to use their listed securities effectively in cross-border M&A deals.

Further, the lack of depth and trading volumes of Indian securities and concerns around the regulatory regime for foreign investors meant that foreign investors were reluctant to accept Indian securities as consideration. Previous attempts by Indian regulators and companies, particularly in the technology sector, to create international securities through ADR/GDR programmes as acquisition currency failed miserably due to low trading volumes.

Indian regulations now allow the swap of Indian shares for foreign securities, significantly easing the process of structuring cross-border deals

Emerging trends and regulatory changes

Despite these challenges, recent regulatory changes and evolving market dynamics offer promising avenues for cross-border M&A involving Indian companies.

Permitting swaps of Indian shares for foreign securities: Indian regulations now allow the swap of Indian shares for foreign securities, both through primary and secondary issuance, at fair market value determined in accordance with international valuation principles, and without requiring regulatory approvals. This development significantly eases the process of structuring cross-border deals, enabling a more flexible and innovative transaction framework which should now allow more combinations of Indian and non-Indian businesses, without needing cash payouts.

Acceptance of Indian securities by international players: There is a growing willingness among international parties, such as private equity firms and strategic investors, to accept Indian securities in cross-border M&A transactions. This is because many of the global private equity, venture capital, pension and sovereign wealth funds have exposure to Indian markets through other investments in India. It is also due to the significant expansion of the free float—which reached US$1.1 trillion market cap in September 2024, out of US$2 trillion in total—and trading volumes on the Indian stock market. This gives international parties accepting Indian securities exposure to the continued increase in those companies’ valuations, as well as the comfort of knowing they can very easily monetise their holdings when they exit.

This acceptance opens up new possibilities for Indian companies to use their high-value securities as currency in international acquisitions, thereby enhancing their global footprint.

Listing Indian securities on international stock exchanges: In January 2024, the Indian government announced that it would permit Indian companies, both listed and unlisted, to list their securities on international stock exchanges. This will further encourage Indian companies to create securities that have greater acceptance with shareholders of international targets.

Potential for new deal structures

These regulatory changes and market developments set the stage for interesting deal structures that could invigorate cross-border M&A involving Indian companies. A few potential deal structures include:

Mix of cash and share swaps: In this scenario, foreign acquirers purchase India-listed companies with a mix of cash for the public shareholders and share swaps for the controlling or larger shareholder, leveraging the regulatory flexibility now offered for secondary share swaps. This allows the deal structure to balance public shareholder interests, as required by Indian securities law, while controlling shareholders have the flexibility of continuing to participate in the combined business by accepting share consideration.

Genuine combinations and mergers of equals: Here, Indian and foreign entities join to create global leaders in their sector without the need to take on significant leverage.

Reverse flip structures: This structure involves the non-Indian businesses, both of third parties and their parent company, being acquired by Indian subsidiaries of global companies without needing to pay cash.

Using high-valuation securities to acquire foreign assets: This set-up allows Indian companies to make cross-border investments without having to leverage themselves with USD debt, thereby expanding their global presence and operational capabilities.

Outlook

The high-valuation multiples of Indian companies present both opportunities and challenges in the M&A landscape. While regulatory and market barriers have complicated cross-border transactions, recent developments offer the potential for more dynamic and innovative deal structures. As Indian regulations continue to evolve and international investors become more receptive to Indian securities, the prospects for cross-border M&A involving Indian companies appear increasingly promising. This could lead to a significant boost in global dealmaking activity, benefitting both Indian and international markets.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: PE ratios of India-listed companies – Nifty Indices (PDF)

View full image: PE ratios of India-listed companies – Nifty Indices (PDF)