Global IPO market overview

Global IPO proceeds improved in 2024, but while some IPO markets performed strongly, others faced a challenging year. In 2025, regional markets appear set to drive IPO themes

Global IPO markets delivered improved year-on-year performance in 2024, with some regions contributing more than others. The outlook for 2025 remains broadly positive, although an escalating trade tariff standoff among certain major economies could weigh on activity

After an incredibly challenging two years, global IPO markets are back on an upward trajectory.

Falling interest rates in key markets encouraged IPO candidates to come to market in 2024, resulting in a five percent jump in year-on-year IPO proceeds. Momentum has carried into the early months of 2025. In the US, liquefied natural gas exporter Venture Global raised US$1.75 billion from its IPO, Chinese bubble tea maker Mixue landed a US$444 million IPO in Hong Kong and, in Amsterdam, luxury logistics company Ferrari Group performed well in early trading after listing at a market capitalization of US$818 million.

However, the headlines do not tell the full story, as global activity was driven by very local themes. While some IPO markets thrived, others had a more challenging year.

India and the Middle East were the two standout regions for IPOs in 2024. India consolidated its position in 2024 as the busiest IPO market in the world by deal count, while the Middle East delivered large, groundbreaking listings.

The US and Europe saw improved annual IPO issuance as interest rates decreased. But they still have some ground to make up to get back to pre-pandemic activity levels.

In other regions, launching new listings has been challenging. In China, domestic economic headwinds have put the brakes on IPOs on mainland stock exchanges, although Chinese issuers have been able to proceed with listings on Hong Kong and US exchanges. Meanwhile, in Latin America, activity has been hampered by sustained high interest rates in the crucial Brazilian market.

As 2025 unfolds, this regional patchwork of localized themes looks set to continue shaping the global picture.

The macroeconomic environment for IPO activity is significantly more supportive than it was a year ago, as interest rates appear to have peaked. However, the impact of the United States’ tariff policy will be felt across global markets. The US has imposed and rescinded tariffs on various trading partners, creating uncertainty for investors and supply chains.

IPO opportunities should continue to emerge in 2025, but in a more complex world, investors will be analyzing developments in global trade and using a regional lens to identify the best IPO deals.

Global IPO proceeds improved in 2024, but while some IPO markets performed strongly, others faced a challenging year. In 2025, regional markets appear set to drive IPO themes

US IPO markets entered 2025 well positioned for a promising year as stabilizing interest rates, a business-friendly US administration and the pressing need for private equity firms to exit portfolio companies laid the foundation for a favorable IPO environment, but uncertainty regarding US tariffs and retaliatory actions by other nations, and continuing market volatility have weighed on early offering

Although European IPO markets still trail pre-pandemic levels, they began an upward trajectory in 2024, with an encouraging pipeline of new IPO candidates lined up for 2025. Regulators, issuers and investors are not resting on their laurels and continue to sustain long-term growth and competitiveness

The Asia-Pacific region had to contend with a slowdown in new listings in mainland China, but another bumper year for India's IPO market, which consolidated its position as the most active IPO hub globally, helped to lift overall activity in the region

Long-term policy initiatives supporting the development of capital markets in the Middle East are paying off, with stock markets across the region supporting a cluster of large state-backed and private sector IPOs in 2024

Although Latin America IPO markets look set to remain challenging in the year ahead, investors who are able to handle risk will find opportunities

Global IPO activity showed steady progress in 2024. Although geopolitical volatility still lingers, the foundations are in place for another solid year

The Asia-Pacific region had to contend with a slowdown in new listings in mainland China, but another bumper year for India's IPO market, which consolidated its position as the most active IPO hub globally, helped to lift overall activity in the region

For the second year in a row, India delivered more IPOs than any country in the world, consolidating its position as the key hub for APAC IPO activity.

India led the world with 338 IPO deals, a 44 percent increase compared to the country's 2023 IPO count. India's IPO proceeds showed even stronger gains, increasing almost threefold from US$7.9 billion in 2023 to US$20.99 billion in 2024. Only the United States posted higher IPO proceeds.

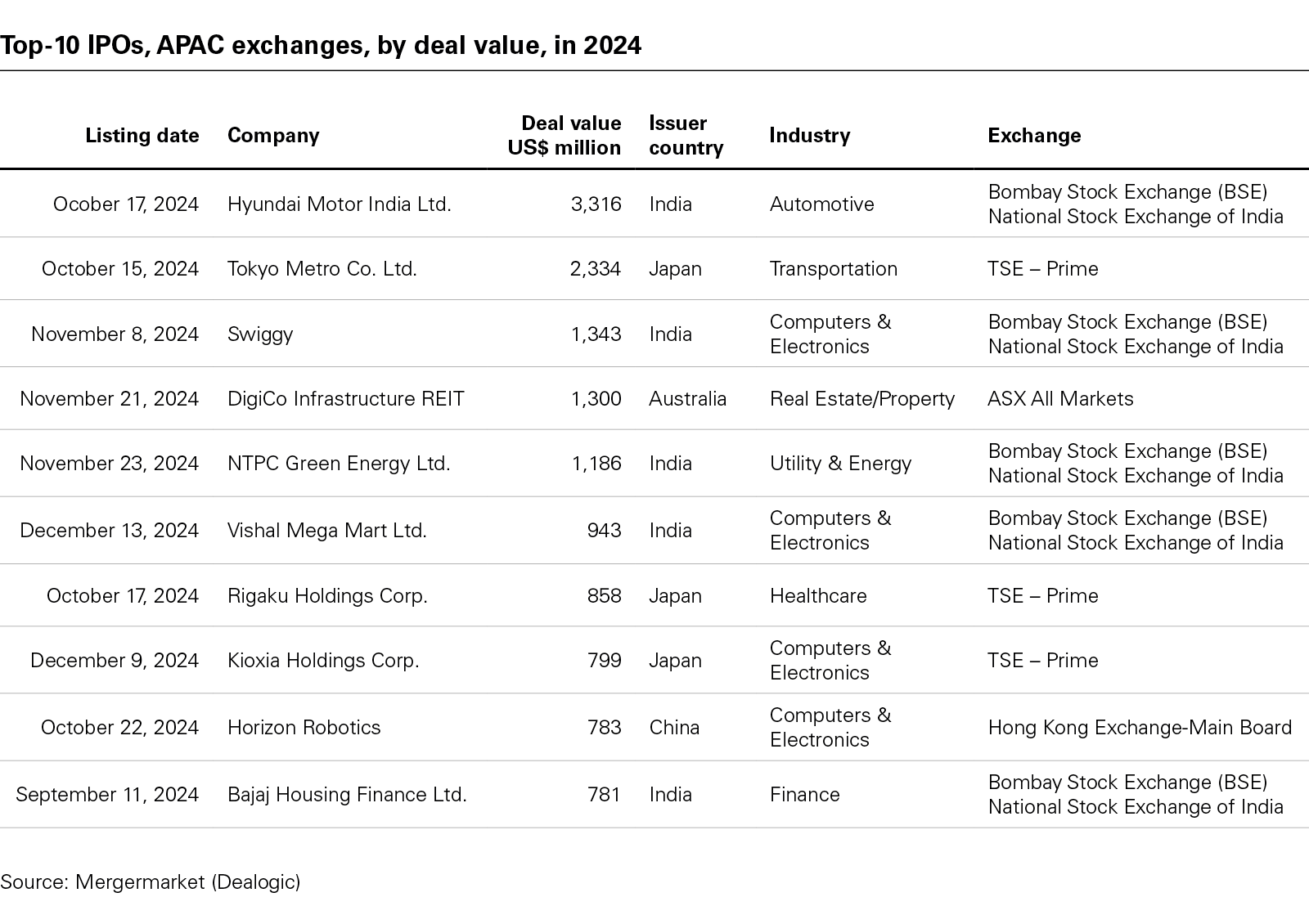

Notably, South Korean car marker Hyundai floated its Indian subsidiary in an IPO that raised US$3.3 billion, exemplifying the growing depth and sophistication of India's IPO markets, which not only have the capacity to process a high volume of IPO deals but can also now finance large IPOs of a significant scale.

Hyundai's India subsidiary's listing was ranked both the second-largest IPO in the world and the largest-ever Indian IPO. A decade ago, an IPO of this magnitude would have had to look to foreign stock exchanges to secure the necessary capital, but after years of consistent expansion, India's stock exchanges are now more than capable of financing jumbo listings.

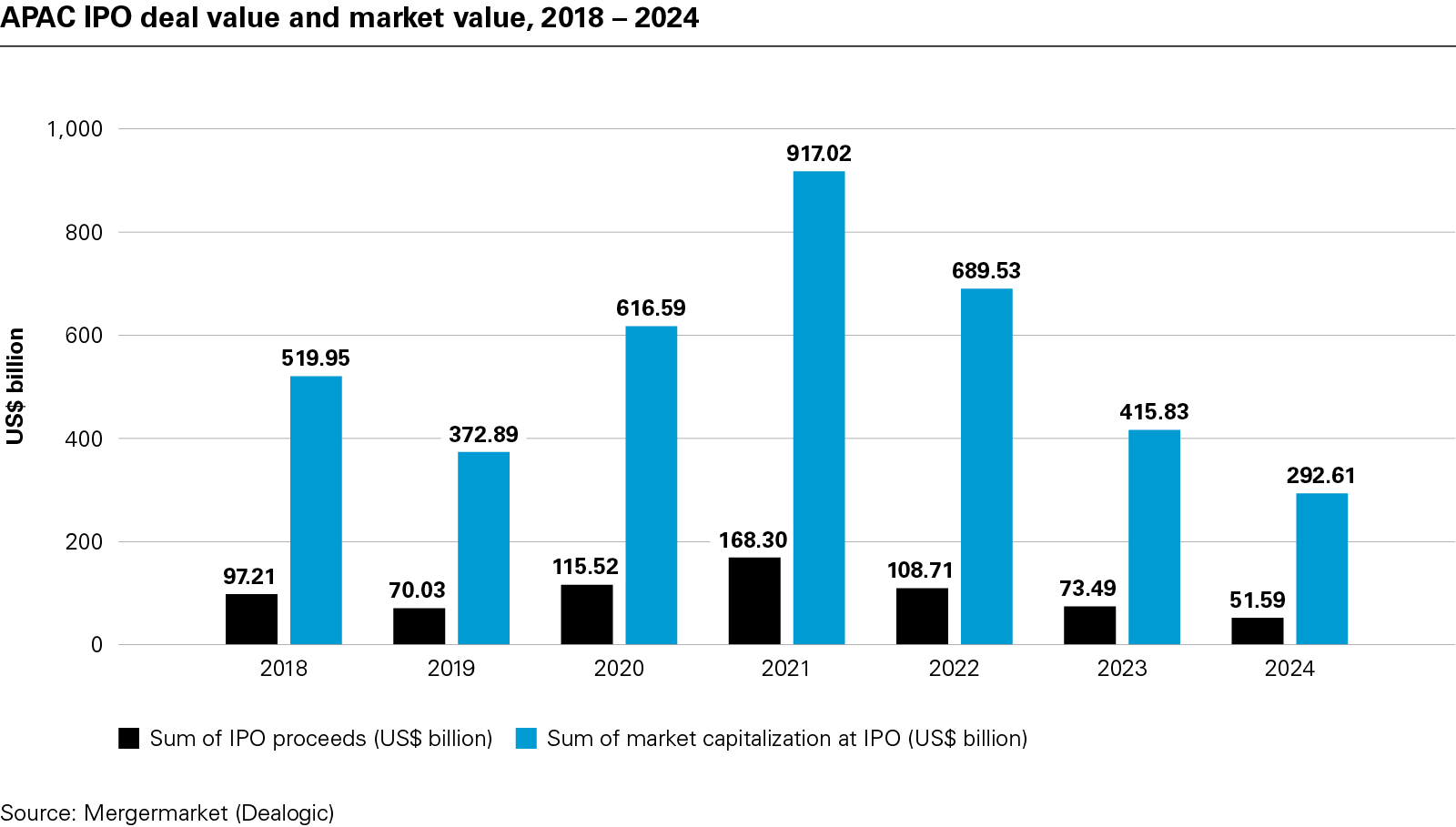

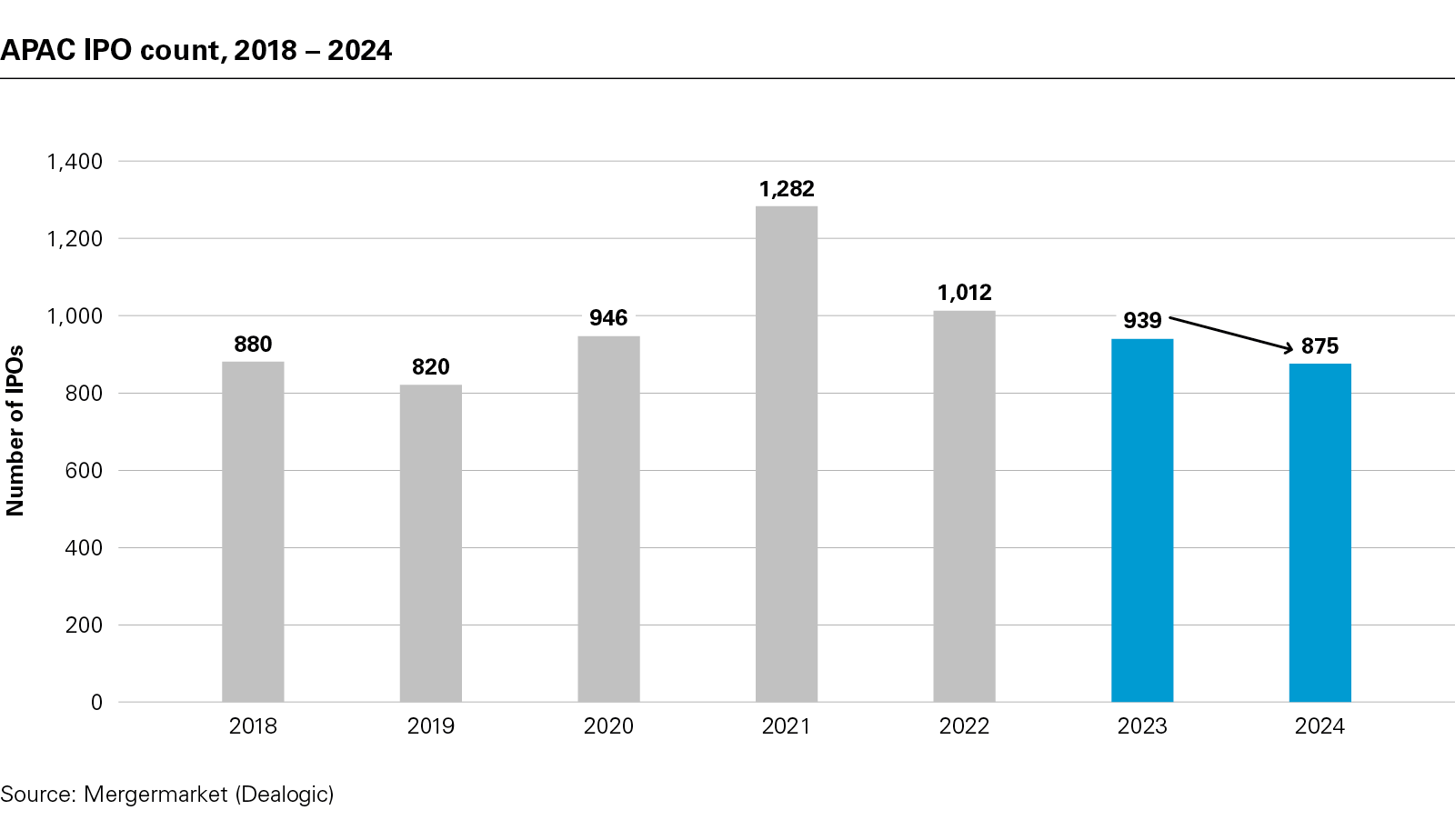

While India was the standout performer in APAC, IPO activity in other major regional jurisdictions was mixed. Overall, APAC IPO proceeds dropped to US$51.59 billion in 2024 from US$73.49 billion in 2023, with the IPO count dropping to 875 IPOs in 2024 from 939 deals in 2023. This was mainly due to a sharp slide in IPO proceeds in mainland China, although Hong Kong saw a small uptick in year-on-year IPO issuances.

Indonesian IPO proceeds dropped significantly when compared to 2023, with an election in 2024 putting the brakes on activity, and IPOs in Singapore were flat.

Early in 2025, APAC IPO activity has been steady, with 57 IPOs raising US$2.76 billion in January 2025 compared to the US$2.96 billion raised from 63 IPOs in January 2024.

The robust Indian IPO market has been supported by strong economic growth. The Organization for Economic Cooperation and Development forecasts that GDP will increase by approximately 6.8 percent in the 2024 – 2025 fiscal year and sustain this level of growth into 2027.

Indian IPOs also have benefited from the rapid expansion of the domestic retail investor base, as household investment into local equity markets surges. This democratization of investment in India drove triple-digit inflows into Indian mutual funds in 2024, according to ICRA Analytics, deepening the pools of liquidity available for investment in new listings.

Deeper liquidity has seen India able to support jumbo IPO deals. In addition to the landmark Hyundai IPO, other successful large-cap IPOs in India included food and grocery delivery business Swiggy, which raised just under US$1.4 billion in its market debut, and NTPC Green Energy, the renewable energy division of state-owned power company NTPC, which raised US$1.18 billion from its IPO. Market momentum seems poised to continue in 2025, with more large IPOs in the pipeline for the year ahead.

The growing number of US$1 billion-plus IPOs in India could also see Indian companies, particularly technology businesses that originally listed in the US or Europe in order to tap into liquidity and obtain higher valuations, move their listings back to an increasingly mature, more liquid and more sophisticated Indian market that can now deliver large sums of capital at attractive valuations.

The pace of new listings in China slowed down significantly year-on-year in 2024, primarily as a result of tighter IPO regulations implemented in the first half of 2024, coupled with the challenges posed by an economy that continued to be affected by the fallout from a liquidity squeeze in its key real estate sector—accounting for approximately a fifth of China's economy—among other things. The value of IPO proceeds on mainland China exchanges fell from US$45.92 billion in 2023 to just US$8.62 billion in 2024.

On the other hand, Hong Kong IPO activity held steady, with IPOs raising proceeds in the amount of US$5.88 billion in 2024 compared to the US$5.74 billion the previous year, as many Chinese issuers, faced with a challenging IPO market in the mainland, turned to listing venues outside of mainland China, including Hong Kong and the US. Although IPO activity in mainland China and Hong Kong was generally muted in 2024, equity capital markets have remained open for business, with Bloomberg noting a 40 percent increase in dollar-denominated convertible bond issuances in 2024 as compared to 2023.

Indeed, Hong Kong has had a strong start to 2025. Chinese bubble tea maker Mixue landed a US$444 million IPO, while Chinese electric vehicle company BYD raised US$5.59 billion, boosting optimism that 2025 could see a strong upswing for Hong Kong IPOs and capital raisings.

Chinese issuers have reason to hope that 2025 will see China IPO activity increase its share of equity capital markets activity in APAC, as the market absorbs the impact of the new regulatory regime, investors seize opportunities to invest in assets at attractive valuations and economic growth stabilizes. The market has also reacted positively to the various government support and market stimulus measures announced by the Chinese government in the second half of 2024.

However, uncertainties persist, including those related to geopolitical tensions, which could pose headwinds to growth.

Investors, issuers and advisers are hopeful that Indonesia will see stronger IPO activity in 2025, after a slow 12 months in which an election, the formation of a new government, high interest rates in the US and slower than expected growth in China, among other factors, saw issuers and investors take a "wait and see" approach on their IPO plans.

Indonesia's economic fundamentals position the country as one of the most attractive growth markets in the world. Indonesia is the largest economy in Southeast Asia and is set to benefit from a sizeable young population, with a little more than half of its 270 million population under the age of 40.

Historically, Indonesia's IPO market has been resilient, but Indonesian IPO proceeds slid from US$3.54 billion in 2023 to just US$895 million in 2024. With elections completed and the new government formed, 2025 is anticipated to see an increased pipeline of issuance activity.

However, it remains to be seen if this uptick will be gradual or rapid, and challenges remain given geopolitical uncertainties. Nonetheless, Indonesia benefits from a growing middle class, providing a strong consumer base, and an economy that is diversifying beyond its core commodity base into other areas such as EV, technology and digital infrastructure.

The recent passing of a law to form a new sovereign investment vehicle called Danantara could also have a significant impact on Indonesia's capital markets. The entity will oversee the management of more than US$60 billion in state assets, taking the lead on consolidation and value creation for state-owned businesses. It will also have the flexibility to make direct and indirect investments and partner with third-party investors.

This is a significant development for the Indonesian economy and will be an area for investors to keep a close eye on throughout 2025.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP

View full image: APAC IPO deal value and market value, 2018 – 2024 (PDF)

View full image: APAC IPO deal value and market value, 2018 – 2024 (PDF)

View full image: APAC IPO count, 2018 – 2024 (PDF)

View full image: APAC IPO count, 2018 – 2024 (PDF)

View full image: Top-10 IPOs, APAC exchanges, by deal value, in 2024 (PDF)

View full image: Top-10 IPOs, APAC exchanges, by deal value, in 2024 (PDF)