Financial institutions M&A: Sector trends - September 2024

Financial institutions M&A: Sector trends

We highlight the key UK & European M&A trends in H2 2023 and H1 2024, and provide our insights into the outlook for M&A moving forward.

Introduction

In the 12th edition of our report, we bring you the key deal highlights and M&A trends across UK/Europe in the past 12 months which have shaped the financial services landscape. Focusing on the following verticals:

Key highlights include:

Banks: Europe’s banks restructure, consolidate and partner their way into the digital future.

Fintech: Tepid UK & European private capital markets spur unicorns into inorganic opportunities.

Asset/Wealth Management: Europe’s barbell becomes more pronounced—larger asset/wealth managers swallow smaller competitors at pace.

Payments: Equity and debt cheques from financial sponsors fuel growth, with investment committee appetite across the full spectrum from Seed through to late-stage/pre-IPO. The payments sector bucks the trend on IPOs.

Brokers/Corporate Finance: Mid-market investment banks consolidate at the fastest rate yet—reshaping the City skyline.

Consumer Finance: Inflexion point arrives for UK & European consumer lending. The strong will survive as BNPL and POS finance become the norm for e-commerce.

Specialty Finance/Marketplace Lending: Consolidation fever grips non-bank lenders and banks alike—SME lending, revenue-based finance and PropFinance at its core.

European financial services M&A trends

Europe’s banks restructure, consolidate and partner their way into the digital future

Equity and debt cheques from financial sponsors fuel growth, with investment committee appetite across the full spectrum from Seed through to late- stage / pre-IPO. The payments sector bucks the trend on IPOs.

Mid-market investment banks consolidate at the fastest rate yet— Panmure Gordon & Liberum, Redburn (Europe) & Atlantic Equities and Cenkos Securities & FinnCap Group mergers reshape the City skyline.

3 reasons for continuously high fintech M&A activity levels:

Banks target indirect digital access: Through credit lines, investments in venture capital funds, collaborations with innovators and establishment of next generation incubators.

No shortage of asset availability: Financial sponsors seizing exit opportunities, fintechs shedding non-core business lines and banks cashing-out.

Thinning of the herd: Private capital drought claims its first victims—overcrowded consumer finance and payments verticals yield the most casualties.

Current market

UK & European private capital appetite cools— fintechs are forced to restructure and explore other opportunities for growth.

We are seeing

Banks double-down on digitalisation:

Acquisitions of digital distribution channels (e.g., Crédit Agricole’s acquisitions of Pledg and Worklife)

Equity investments into software providers (e.g., Emirates NBD’s equity investments in Erguvan and Komgo)

Venture fund investments—Citi Ventures one of the most active in the last 12 months (e.g., participation in funding rounds for Colendi, TUUM, PPRO, Defacto and Komgo)

Partnerships with digital asset tech providers (e.g., Deutsche Bank’s customer deposits & withdrawals JV with Bitpanda and €-denominated stablecoin JV with Galaxy Digital / Flow Traders)

Development of ‘home grown’ technology, both directly (e.g., Garanti BBVA’s launch of Bonus Platinum Biometric Card) as well as through venture arms (e.g., Standard Chartered’s / SC Ventures’ launch of SOLV Ghana) and via partnerships (e.g., HSBC’s launch of Zing in collaboration with Visa)

Banks gain access indirectly through:

Credit lines (e.g., Deutsche Bank’s £100 million securitised debt financing for Zilch and JP Morgan’s US$700 million debt funding for Tabby)

Investments in venture capital funds (e.g., Raiffeisen’s investment in Elevator Ventures’ €70 million venture capital fund, EV II)

Collaborations with innovators (e.g., BNP Paribas’ launch of Panto, in partnership with Startup Studio 321, and BNY Mellon’s launch of Alpheya, in partnership with Lunate)

Establishment of next generation incubators (e.g., BNP Paribas’ launch of UK innovation lab, in partnership with SuperTech)

As ‘big name’ VCs cherry-pick investment opportunities, fintechs rely heavily on debt:

Mixed equity and debt funding rounds: both early stage (e.g., Zanifu’s US$11.2 million pre-Series A debt & equity funding round) and late stage (e.g., Abound’s £800 million debt & equity funding round)

Debt funding from venture capital sponsors: predominantly early-stage (e.g., TRIVER’s €22.9 million debt facility from Avellinia Capital and Multifi’s £10 million debt funding round led by Fasanara Capital)

Debt funding from specialist providers: predominantly mid-stage (e.g., Kriya’s £50 million debt financing from Viola Credit)

Credit lines from established banks: predominantly late-stage (e.g., Barclays’ £200 million debt funding for iwoca)

Established / mature fintechs pivot:

Merger with compatible competitors (e.g., merger of Trustly and Slimpay)

Acquisition of competitors (>35 significant consolidation deals in the last 12 months)

Strategic tie-ups to scale-up (>25 significant partnerships in the last 12 months)

Entry into new verticals (e.g., SumUp’s launches of POS Lite and Cash Advance services)

Operational stress fractures come to the fore:

Corporate shake-ups (e.g., Monese & XYB and Bitpanda & Bitpanda Pro / One Trading de-mergers

Wind-downs—overcrowded consumer finance vertical (e.g., Divido, Laybuy, Fronted, ZestMoney and Koyo Loans shut shop) and payments vertical (e.g., Silverbird, Twig, Kikapay, Paysme and Cardeo shut shop) claim the most victims

New tech—all cheque sizes (e.g., Cloover’s US$114 million Seed funding round, Portal’s US$34 million Seed funding round and Spektr’s €5 million Seed funding round)

Fintechs penetrating new geographic markets— number of African fintech start-ups grew by 17.7% in the last 24 months, with Nigeria, Egypt, Kenya and South Africa dominating

Pressure is mounting on PE / VC investors to return capital to their LPs. While market appetite for IPOs remains luke warm, portfolio businesses are under pressure to deliver exits in other ways—that’s a key driver behind consolidation in the UK & European fintech sector.

Guy Potel

Key drivers

Financial sponsors sign equity cheques for:

Well-known brands, evidencing clear pathway to profitability / exit:

Hottest fintech verticals for fundraising activity in the last 12 months:

3rd | SME lending: >10 successful fundraisings, including:

Finiata’s €20 million late-stage equity funding round

FINOM’s €50 million Series B funding round

Defacto’s €10 million Series A+ funding round

Search for scale drives fintech M&A activity:

Hottest fintech verticals for fundraising activity in the last 12 months:

Acquisitions

1st | Trading & data analytics: Selection of market examples, including:

Access Group’s acquisition of Lightyear

Lesaka’s acquisition of Touchsides

Levenue’s acquisition of Cake

2nd | Payments: Selection of market examples, including:

Spendesk’s acquisition of Okko

GSTechnologies’ acquisition of 60% of EasySen

OPay’s acquisition of FINJA

3rd | InsurTech: Selection of market examples, including:

BSI’s acquisition of riskine

bolttech’s acquisition of Digital Care

Getsafe’s acquisition of Luko’s German business

Hottest fintech verticals for consolidation activity in the last 12 months:

Partnerships

1stPayments | Selection of market examples, including:

Thought Machine’s core banking JV with Mastercard

Airwallex’s global payments JV with Bird

StoneX Payments’ cross-border payments JV with NatWest

2nd RegTech | Selection of market examples, including:

Nium’s payments compliance JV with Trulioo

Kaizen’s regulatory reporting JV with Berenberg

Symphony’s financial markets voice analytics JV with Google

3rdWealthTech | Selection of market examples, including:

Lunate’s MENA wealth management technology JV (Alpheya) with BNY Mellon

WealthOS’s technology partnership with Quai Digital

FusionIQ’s a mutual referral partnership with interVal

Continued interest in fintech M&A opportunities by myriad of investors, including:

Corporates searching for complementary client bases, capabilities and experience (e.g., Alpha Group’s acquisition of 85% of Cobase)

UHNWs searching for investment returns (e.g., Sheikha Amal Suhail Bahwan’s acquisition of equity stake in Monument Bank)

SWFs searching for opportunities to deploy state funds (e.g., GIC’s participation in Monzo’s US$190 million late-stage funding round)

No shortage of asset availability:

JV participants dissolve partnerships (e.g., Saxo Bank’s sale of its stake in Saxo Fintech to Geely Group)

Financial sponsors seizing exit opportunities (e.g., CDP Venture Capital’s and Digital Magics’ disposal of Axieme)

Incubators running their course (e.g., Deloitte’s disposal of UK RegTech business)

Fintech decacorns getting race fit (e.g., Klarna’s disposal of Hero and Klarna Kosma)

Banks cashing-out (e.g., ING’s disposals of CoorpID, Blacksmith KYC and Cobase)

Trends to watch

Greater number of transactions, but smaller ticket— more fintechs willing to close funding rounds earlier in the hope of more favourable conditions for extension rounds

Uptick in consolidation activity as fintechs combine to weather scrutiny of financial sponsor investment committees—expect more “paper only” deals

Governments, regulators and politicians play a vocal role in fintech development:

Differing views on BigTech within financial services: policy-makers provide support (e.g., U.S. and UAE governments’ support of Microsoft’s acquisition of US$1.5 billion interest in G42), while regulators express scepticism (e.g., UK FCA’s investigations into competitive implications of BigTech)

Improving sentiment towards digital assets: embrace of securities tokenisation (e.g., key aim of UK Labour Party) and right-sizing of regulation (e.g., UK Treasury’s rejection by all-party parliamentary committee’s proposals for consumer trading in unbacked crypto to be regulated as gambling)

Approach to deployment of government-backed funding: government funds invest directly into start¬ups, both advanced-stage (e.g., Folketrygdfondet’s participation in €82 million funding round in Ageras) and early-stage (e.g., Flemish Welfare Fund’s participation in €11.5 million funding round in Lizy)

Our M&A forecast

Europe’s fintech ecosystem has matured significantly in the last year, and will continue to do so in the next year.

Expect equity funding to remain challenging, with onerous / prescriptive terms around down-round protection, exit timing and use of proceeds becoming the norm. We expect an increasing willingness within the fintech community to accept debt alternatives or turn to credit lines from banks.

It seems inevitable that a greater number of fintechs will be forced out of the market—but that creates opportunity for those which survive!

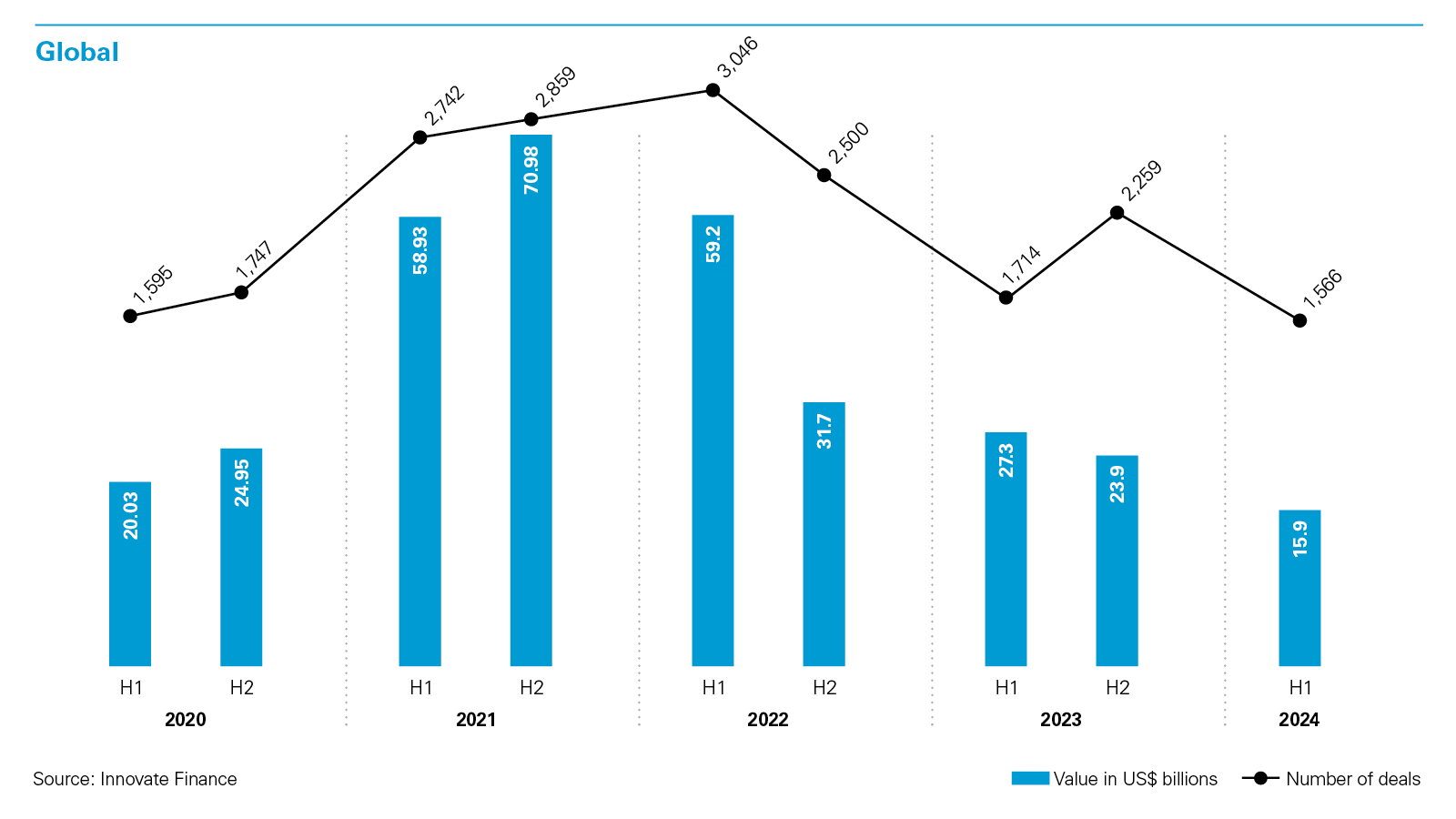

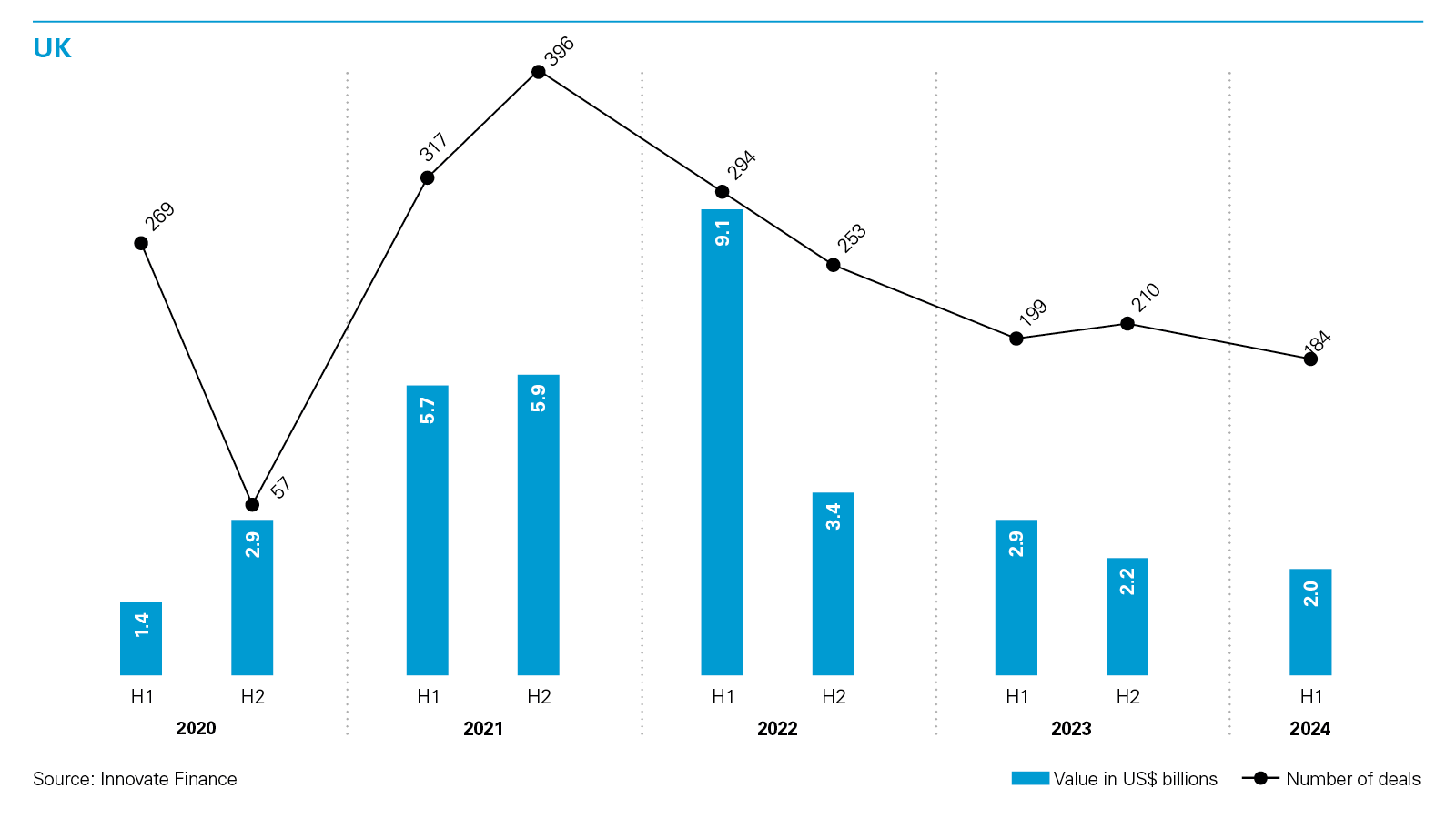

5-year fintech funding landscape

Set out below are diagramatic illustrations of the volume of capital raised, as well as number of fundraising deals executed, by fintechs over the last 5 years.

5 key investor rights for 2024 – What you need to know

Overview

Liquidation preference

How does it work?

The incoming investor receives a contractually agreed preferential payout if / when the investee company experiences a “liquidity event” (such as a sale or IPO).

Why is it used?

Liquidation preferences are used to grant an incoming investor a higher priority of return than an existing investor, when calculating returns at exit (the typical VC / growth model is “last in, first out”).

How common is it?

1x non-participating liquidation preferences (where the investor will receive the higher of the amount invested and their pro rata share of the invested company) are still the norm (especially for early stage), but we are beginning to see later stage investors insist on higher liquidation preferences.

In the current market climate, we are seeing enhanced liquidation preferences (even with up to 3x return). This structuring allows an investee company to avoid a down round (at least, optically) by issuing fresh equity at a flat (or even higher) price per share to the previous funding round, although the incoming investor is not truly taking the risk of the investment at the valuation of the current funding round.

Guaranteed minimum returns

How does it work?

A veto right which prevents an investor from being dragged into an exit which is taking place below a certain threshold return (this is usually tied to the latest investor’s liquidation preference, but can increase over time to capture an expected rate of return).

Why is it used?

Provides an incoming investor with a level of comfort as to the minimum return that it will achieve on its investment (perhaps within a certain timeframe).

How common is it?

Common in the current market climate and often structured as a straight veto. We see this as a blunt instrument and so would recommend replacing it with a “make-whole” concept instead, allowing an exit to proceed below the required threshold provided that the investee company is able to make a make-whole payment to the incoming investor to bring the incoming investor up to the desired threshold.

Anti-dilution rights

How does it work?

A price protection mechanism which is triggered if new shares are issued at a valuation which is lower than that at which an investor originally invested (i.e. a down round). It typically functions by applying a formula to calculate the number of new bonus shares which the investor will receive.

Why is it used?

To protect the value of an investor’s stake in the investee company, by offsetting the dilutive effect of an issue of cheaper shares.

How common is it?

Common in the current market climate. We are also seeing anti-dilution terms introduced at an earlier stage (i.e. Seed and Series A), given the prevalence of down rounds.

Pay-to-play

How does it work?

Most commonly, this will operate by:

the investee company issuing a large number of new shares to the participating investors at a low valuation (resulting in severe dilution to existing shareholdings);

forced conversions of existing preferred shares;

a share split; or

the issue of a new class of preference shares to participating investors with a very high senior preference.

Why is it used?

It acts as an incentivisation to existing investors to participate in a new financing round, either by negatively impacting investors who opt not to participate or rewarding investors who choose to participate.

How common is it?

Very common in the current market climate. We are increasingly seeing companies explore “cram down” financings.

A “cram down” financing is new financing with terms significantly dilutive to non-participating investors, which are typically structured on a pay-to-play basis, led by one or more of the investee company’s existing investors and, in the most severe cases, will result in non-participating investors ending up with little to no ownership stake following the funding round (or no meaningful prospect of a return on their investment).

Initially, post the 2022 downturn, companies were reluctant to accept the consequences of a “cram down” and instead opted to subscribe for convertible loan notes or other instruments which deferred valuation debate. However, companies are now realising they need to “fix” their capital structure if they want to incentivise employees and attract third party financing.

Redemption rights

How does it work?

Right to demand, under certain conditions, that the investee company redeems / buys back its own shares from its investors at a fixed price.

Why is it used?

This right may be included to require an investee company to redeem / buy back its shares if there has not been an exit within a pre-determined period, providing the incoming investor with a level of comfort as to the return it will achieve within a certain timeframe.

Failure to redeem shares when requested might result in the incoming investor gaining improved rights, such as enhanced voting rights. A right of redemption can also be used by an incoming investor where it needs to strongly discourage an investee company from breaching certain obligations, by enabling a quick disposal of shareholding.

How common is it?

A right of redemption / buy back is not appropriate for every investment and, in the UK and certain other jurisdictions, there are legal requirements that must be satisfied before a company can redeem / buy back any of its shares.

In jurisdictions where redemption / buy back is not possible under local law, an alternative could be to negotiate a conditional right for the investors to sell their shares to the investee company’s founders at a fixed price.

Fintech – Publicly reported deals & situations

Banks adopt multi-channel approach

Market commentary:

43% of European banks are investing in fintech start-ups and 36% are building their own greenfield digital bank or fintech company (Finextra–February 2024).

Nearly half of all banks are looking to buy majority stakes in fintechs to fend off the threat from BigTech (Finextra– November 2023).

Acquisitions:

NatWest: Payments Acquisition of minority stake in Icon Solutions (March 2024)

Crédit Agricole: POS lendingAcquisition of Pledg (February 2024)

BAWAG: Digital banking Acquisition of Knab (February 2024)

Nordiska Kreditmarkn-adsaktiebolaget: SME finance, Acquisition of Release Finans (December 2023)

ABN AMRO Bank: Neo-broking Acquisition of BUX (December 2023)

Dubai Islamic Bank: Digital banking, Acquisition of 20% of T.O.M. Katilim Bankasi (September 2023)

Crédit Agricole: Employee benefits SaaS, Acquisition of Worklife (September 2023)

Equity investments:

Citi: SME lending, AI-powered modular commercial lending platform equity investment in Numerated (June 2024)

Rabobank: RegTech, Participation in Series B+ funding round in Hawk (June 2024)

Bank of Georgia: Digital banking, Participation in US$32 million Series B+ funding round in Fintech Farm (May 2024)

Danske Bank: Digital transformation platform, Equity investment in United Fintech (May 2024)

Zions Bank: Credit-card-as-a-service Participation in US$85 million Series C funding round in Brim Financial (April 2024)

J.P. Morgan: Payments, Participation in €85 million funding round in PPRO (March 2024)

HSBC: WealthTech, Participation in €12 million Series A funding round in Unbox (January 2024)

JPMorgan Chase: BaaS, Participation in US$45 million funding round in 10x Banking Technology (January 2024)

Groupe BPCE and Crédito Agricola: Personal finance management, Participation in €15 million Series D funding round in Meniga (December 2023)

Citi (Treasury and Trade Solutions): Payments, Equity investment in Icon Solutions (December 2023)

Goldman Sachs: Payments, Participation in £77.7 million Series B funding round in Fnality (November 2023)

BNP Paribas: Payments, Participation in £77.7 million Series B funding round in Fnality (November 2023)

BBVA: Digital banking, Participation in £100 million funding round in Atom Bank (November 2023)

Isbank: Mobile banking, Equity investment of US$50 million in Getir (August 2023)

Emirates NBD: ESGTech, Participation in Seed funding round in Erguvan (September 2023)

Emirates NBD: Trade finance software, Participation in funding round in Komgo (September 2023)

HSBC: Supply chain finance, Participation in US$35 million funding round in Tradeshift (August 2023)

BBVA: Embedded finance, Participation in €38 million Series F funding round in Solaris (July 2023)

Santander: Trade finance software, Participation in equity funding round in Komgo

Partnerships:

Deutsche Bank: Crypto, Customer deposits and withdrawals JV with Bitpanda (June 2024)

NatWest: Payments, Cross-border payments JV with StoneX Payments (April 2024)

Berenberg: RegTech, Regulatory reporting JV with Kaizen (January 2024)

National Bank of Oman: B2B payments, B2B payments JV with PayMate (January 2024)

BNY Mellon: WealthTech, MENA wealth management technology JV (Alpheya) with Lunate (November 2023)

SC Ventures (Standard Chartered): Digital assets, Digital asset JV with SBI Holding (November 2023)

BNP Paribas: Payments, Marketplace payments JV (Panto) with Startup Studio 321 (October 2023)

Isbank: Mobile banking, BaaS JV (GetirFinans) with Getir (October 2023)

Venture fund investments:

NAB Ventures: Digital asset custody, Equity investment in Zodia Custody (June 2024)

CommerzVentures and UBS: ClimateTech, Participation in €34 million Series B funding round in Doconomy (May 2024)

Citi Ventures: Digital banking, Participation in US$65 million funding round in Colendi (May 2024)

Citi Ventures: Core banking platform, Participation in Series B+ funding round in TUUM (March 2024)

Citi Ventures: Payments,Participation in €80 million funding round in PPRO (March 2024)

Commerz Ventures: Core banking platform, Participation in €25 million Series B funding round in TUUM (February 2024)

Citi Ventures: SME lending, Participation in €10 million Series A+ funding round in Defacto (November 2023)

ABN AMRO Ventures: SaaS, Participation in €30 million funding round in Upvest (October 2023)

Citi Ventures: Trade finance software, Participation in funding round in Komgo (September 2023)

Debt funding:

Deutsche Bank: BNPL, Arrangement of £100 million securitised debt financing in Zilch (June 2024)

Citigroup: Consumer credit, Debt participation in £800 million debt and equity funding round in Abound

Goldman Sachs: Payments, Participation in €1.5 billion private credit debt funding round in SumUp (May 2024)

Standard Bank: BNPL, Provision of US$10 million growth debt facility to Float Technologies Proprietary (March 2024)

J.P. Morgan: BNPL, Participation in US$700 million debt funding round in Tabby (December 2023)

Barclays Bank: SME lending, Participation in £200 million debt funding round in iwoca (October 2023)

Goldman Sachs and Citibank: SME lending, Participation in £136 million securitised funding round in Fleximize

BBVA Spark: Payroll finance, Participation in €20 million debt funding round in Payflow (September 2023)

Forward-flow arrangements:

Jefferies Financial and Santander CIB: Consumer credit, Participation in £272 million funding round in Updraft, by way of £250 million forward flow (December 2023)

Financial backing for VCs:

Banco Santander, Venture capital, Acquisition of 33% of Seaya Ventures (February 2024)

Dedicated fintech funds:

Raiffeisen Bank International: Investment in Elevator Ventures’ €70 million venture capital fund, EV II, aimed at Series A and Series B fintech investments (April 2024)

Incubators:

BNP Paribas: Launch of UK innovation lab, in partnership with SuperTech, focused on SME apps (January 2024)

Homegrown:

TBC Bank Uzbekistan: Successful US$38.2 million equity investment from TBC Bank Group, EBRD and IFC to launch new AI-enabled capabilities (July 2024)

Standard Chartered /SC Ventures: Launch of Ghanaian B2B online lending marketplace, SOLV Ghana (February 2024)

Garanti BBVA: Launch of Bonus Platinum Biometric Card (February 2024)

HSBC: Launch of Zing global currency conversion app (January 2024)

Emirates NBD: Launch of ENBD X (September 2023)

CaixaBank: Launch of FXWallets (July 2023)

Financial sponsors keep the faith

Deal highlights:

White & Case advised Pollen Street Capital on its multi-layered investment in Wealth Tech niiio.finance, listed on Börse Düsseldorf and the Frankfurt Stock Exchange.

White & Case advised finmid, the Germany-based embedded financing solutions provider, on its Series A funding round, which comprised primary equity investments by Blossom Capital and Earlybird Ventures as well as a secondary sale of shares by existing shareholders.

White & Case advised finmid, the Germany-based embedded financing solutions provider, on its debt funding round structured as an issue of convertible loan notes.

White & Case advised finmid, the Germany-based embedded financing solutions provider, on the issuance of registered senior notes through a Luxembourg special purpose vehicle to Israel-based debt investor Viola.

Market commentary:

Sponsors have been exploring partial exits, continuation funds and dividend recaps as pressure to return capital to LPs mounts (Mergermarket–March 2024).

The fintech market is returning to some sense of normality in terms of valuations after a period in which it “largely lost its head,” according to CEO of Augmentum Fintech (Finextra–November 2023).

Participation in funding rounds:

Alven Capital: InsurTech, Participation in US$15 million Series A funding round in Supercede (June 2024)

EQT and Alpha JWC Ventures: InsurTech, Participation in US$35 million Series A funding round in Peak3 (June 2024)

BOND, NewView Capital and Tribe Capital: Payments, Participation in US$50 million Series E funding round in Nium (June 2024)

Dawn Capital: InsurTech, Participation in £15 million funding round in Bondaval (May 2024)

Paypoint: Open banking, £1 million equity investment in Aperidata (May 2024)

Well street: ClimateTech, Participation in £1.1 million funding round in Deedster (May 2024)

Lowercarbon Capital: ClimateTech, Participation in US$114 million Seed funding round in Cloover (May 2024)

Migros Ticaret, Sepil Ventures, Re-Pie Asset Management, Finberg and Hedef Holding: Digital banking, Participation in US$65 million funding round in Colendi (May 2024)

KKR and Hannover Digital Investments: Payments, Participation in US$93 million Series C funding round in Vitesse (May 2024)

Spark Capital, Dawn Capital, King River Capital and G Squared: InsurTech, Participation in US$80 million Series E funding round in Cover Genius (May 2024)

Nordstar: Digital banking, Participation in US$32 million Series B and B+ funding round in Fintech Farm (May 2024)

Capital G and Hedosophia Digital banking: Participation in US$190 million funding round in Monzo (May 2024)

Idékapital: InsurTech, Participation in funding round in Simplifai (May 2024)

GSR Ventures and Hambro Perks: Consumer credit, Equity participation in £800 million debt and equity funding round in Abound (May 2024)

Investcorp and Lazard: SaaS, Participation in €82 million funding round in Ageras (April 2024)

Portage, International Finance Corporation, Spark Capital, Earlybird Digital East Fund and Revo Capital, WealthTech, Participation in US$45 million funding round in Midas (April 2024)

Dawn Capital and Seed Capital Denmark: Payments, Participation in €45 million Series B funding round in Flatpay (April 2024)

Blossom Capital and Earlybird VC: Embedded finance, Participation in €35 million funding round in finmid (April 2024)

ICONIQ Growth, BDT & MSD Partners and World Innovation Lab: Accounting SaaS, Participation in US$100 million Series E funding round in FloQast (April 2024)

EDC Investments, Vistara Growth, White Owl Group and Epic Ventures: Credit-card-as-a-service, Participation in US$85 million Series C funding round in Brim Financial (April 2024)

ICONIQ Growth: Accounting technology, Participation in US$100 million Series E funding round in FloQast (April 2024)

Key1 Capital: AI fund management, Participation in US$100 million Series C funding round in FundGuard (March 2024)

Mubadala Investment, The Latest Ventures, Africinvest, Palm Drive Capital, Triatlum Advisors and Future Africa: Automobile finance, Participation in US$100 million Series B funding round in Moove (March 2024)

Teachers’ Venture Growth: B2B SaaS, Participation in US$80 million funding round in Perfios (March 2024)

CapitalG, Hongshan Capital, Google Ventures, Tencent and Passion Capital: Digital banking, Participation in US$430 million funding round in Monzo (March 2024)

Crestline Investors: RegTech, Participation in £45 million funding round in Napier AI (February 2024)

Northzone and General Catalyst: SME finance, Participation in €50 million Series B funding round in FINOM (February 2024)

Motive Partners, Unusual Ventures and Bain Capital: Embedded payments, Participation in US$14 million Series B funding round in Navro (February 2024)

KuCoin Ventures: Crypto infrastructure, Participation in equity funding round in Ta-da (February 2024)

TruStage Ventures and Curql Collective: Mobile banking technology, Participation in US$7.7 million Series A funding round in Pulsate (February 2024)

Sequoia Capital and DST Global: Accounting technology, Participation in €40 million Series C funding round in Pennylane (February 2024)

Northzone, Seedcamp and PreSeed Ventures: RegTech, Participation in €5 million Seed funding round in Spektr (February 2024)

Electric Capital: Crypto wallet, Participation in US$10 million Seed+ funding round in Fordefi (February 2024)

OKX Ventures, Arrington Capital, Coinbase Ventures and Gate.io: Crypto wallet, Participation in US$34 million Seed funding round in Portal (January 2024)

Molten Ventures, SBI Investment, Alstin Capital and Motive Ventures: Cards-as-a-service, Participation in €33 million Series A+ funding round in Pliant (January 2024)

VentureFriends, AlleyCorp and u.ventures: Automotive finance, Participation in £15.5 million funding round in Carmoola (January 2024)

Battery Ventures: InsurTech, Participation in US$73 million Series B funding round in Hyperexponential (January 2024)

Portage: WealthTech, Participation in £25 million Series A funding round in ZILO (January 2024)

Maven 11 and Balderton: Crypto custody, Participation in US$15 million funding round in Finoa (January 2024)

Nortia Capital: Neo-banking, Participation in €45 million Series C funding round in MyInvestor (January 2024)

Autotech Ventures: Automotive finance, Participation in €46 million Series B funding round in Bumper (January 2024)

Hassana Investment: BNPL, Participation in US$250 million Series D+ funding round in Tabby (December 2023)

Quilam Capital: Consumer credit, Participation in £22 million funding round in Updraft (December 2023)

SNB Capital and Sanabil Investments: BNPL, Participation in US$340 million Series C funding round in Tamara (December 2023)

Omega EHF: Personal finance management, Participation in €15 million Series D funding round in Meniga (December 2023)

Sanabil Investments: Payments, Participation in US$14 million Series A funding round in Nearpay (December 2023)

13books Capital: Invoice financing, Participation in €15 million funding round in Aria (December 2023)

Bain Capital Tech Opportunities and Sixth Street Growth: Payments, Participation in €285 million debt and equity funding round in SumUp (December 2023)

M&G Investments: Digital asset exchange, Participation in US$30 million Series B funding round in GFO-X (December 2023)

Balderton Capital: WealthTech, Participation in €60 million Series E+ funding round in Scalable Capital (December 2023)

ICONIQ Growth: Trade technology, Participation in US$60 million funding round in Pontera (December 2023)

Maki.vc and Vitruvian Partners: Payments, Participation in €8.5 million Series C+ funding round in Enfuce (November 2023)

Infravia Growth Capital, One Peak Partners and Hermes GPE: Payments, Participation in US$65 million funding round in Paysend (November 2023)

Avellinia Capital: SME / working capital finance, Participation in £20 million funding round in TRIVER (November 2023)

Global Paytech Ventures: Payments, Participation in €15 million funding round in Silverflow (November 2023)

Rockaway Blockchain Fund: Decentralised debt funding platform, Participation in US$60 million funding round in Credix (November 2023)

Ribbit Capital: Payments, Participation in US$75 million Series B funding round in Imprint (November 2023)

Fasanara Capital: Payments, Participation in €34.5 million Seed funding round in Qomodo (November 2023)

Wellington Management: BNPL, Participation in US$200 million Series D funding round in Tabby (November 2023)

Infinity Investment Partners and Toscafund: Digital banking, Participation in £100 million funding round in Atom Bank (November 2023)

eBay Ventures: BNPL, Participation in equity funding round in Zilch (October 2024)

Moneta Venture Capital and D Squared Capital: Embedded finance, Participation in £24 million funding round in Railsr (October 2023)

Fasanara Capital: SME lending, Participation in £10 million debt funding round in multifi (October 2023)

Canapi Ventures: Data analytics, Participation in US$43 million Series C funding round in Nova Credit (October 2023)

Pollen Street: WealthTech, Equity investment in niiio finance (October 2023)

Varde Partners: SME lending, Participation in £200 million debt funding round in iwoca (October 2023)

Mediterrania Capital Partners: Payments, Participation in €57 million funding round in Cash Plus (October 2023)

HV Capital, 10x Capital, Earlybird, Notion Capital and Bessemer Venture Partners: Digital investment platform, Participation in €30 million funding round in Upvest (October 2023)

Fasanara Capital: Decentralised finance, Participation in US$13.5 million funding round in Untangled Finance (October 2023)

HV Capital: SaaS, Participation in US$12.5 million funding round in Kennek (October 2023)

Dawn Capital: Payments, Participation in US$60 million funding round in Brite Payments (October 2023)

Ribbit Capital: Payments, Participation in US$25 million Series A+ funding round in Stitch (October 2023)

Silverstripe Investment Management: Mortgage lending, Participation in US$52 million funding round in Perenna (September 2023)

Index Ventures: SME invoice processing software, Participation in US$15 million Series A funding round in Apron (September 2023)

Britannia, Outward Venture Capital, IDC Ventures, Cohen Circle and Cercano Management: Payments, Participation in £58 million Series C+ funding round in Curve (September 2023)

Susquehanna Private Equity: Pre-paid debit card app for kids, Participation in US$24 million Series A funding round in HyperJar (September 2023)

Serena Capital, Purple. and Motier Ventures: DLT treasury management, Participation in €15 million Seed funding round in Fipto (September 2023)

Lakestar: BaaS, Participation in €37 million Series B funding round in Swan (September 2023)

Silverstripe: Digital banking, Participation in £75 million internal funding round in Zopa (September 2023)

Portage Ventures: RegTech, Participation in US$57 million funding round in ThetaRay (September 2023)

Fasanara Capital: SME lending, Participation in €20 million equity funding round in Finiata (August 2023)

Beyond Capital Ventures and Variant Investments: SME lending, Participation in US$11.2 million pre-Series A debt & equity funding round in Zanifu (August 2023)

Pollen Street Capital: Neo-banking, Participation in €44.5 million funding round in bunq (July 2023)

SoftBank Vision Fund 2: InsurTech, Participation in US$65 million Series E funding round in Tractable (July 2023)

Finleap, Lakestar, Decisive and HV Capital: Embedded finance, Participation in €38 million Series F funding round in Solaris (July 2023)

Quilam Capital: Neo-banking, Participation in £20 million funding round in Tandem (July 2023)

Valar Ventures: Crypto trading, Participation in €30 million funding round in Bitpanda (June 2023)

Venture debt:

CVI Dom Maklerski: WealthTech, Provision of US$12.3 million debt financing to Wealthon (June 2024)

Acquisitions:

TPG and CDPQ: SaaS, Acquisition of equity stake in Aareon (June 2024)

Triple: RegTech, Acquisition of majority stake in SmartSearch (March 2024)

Fasanara Capital: Working capital finance, Acquisition of majority stake in Pollen VC (January 2024)

Amethis: Banking SaaS, Acquisition of majority stake in Capital Banking Solutions (January 2024)

Fundraisings:

Elevator Ventures: EV II, Successful €70 million venture fundraising for Series A and Series B fintech investments (April 2024)

Partech Partners: Partech Venture, Successful €360 million fundraising for dedicated software, data and fintech fund (December 2023)

Northern Gritstone: Investment company, Successful £312 million fundraising for dedicated early-stage fund (October 2023)

Expanding VC capability / capacity:

EMV Capital: Venture capital, Acquisition of Martlet Capital’s VC business (May 2024)

Other FIs double-down on digitalisation

Deal highlight:

White & Case advised Luko, one of Europe’s leading InsurTech providers in the home insurance space, on its sale to Admiral Group, a FTSE100-listed international insurance group.

Verisk Analytics: InsurTech, Acquisition of Rocket Enterprise Solutions (January 2024)

Admiral Group: InsurTech, Acquisition of Luko (October 2023)

Vitanuova: InsurTech, Acquisition of Axieme (September 2023)

Non-Fls cherry pick investment opportunities

Corporates:

Alpha Group: Multi-banking platform, Acquisition of 85% of Cobase (September 2023)

Geely Group: BaaS, Acquisition of Saxo Fintech (June 2023)

UHNWs:

Sheikha Amal Suhail Bahwan: Digital banking, Acquisition of equity stake in Monument Bank (May 2024)

SWFs:

GIC: Digital banking, Participation in US$190 million funding round in Monzo (May 2024)

Dubai Investments: Neo-banking, Participation in £40.6 million Series B funding round in Monument Bank (November 2023)

The wheel of time turns – cashing out

Financial sponsors:

Advent: SaaS, Disposal of equity stake in Aareon (June 2024)

Stemar Capital, Runa Capital and Mazovia Capital: InsurTech, Disposal of Digital Care (October 2023)

CDP Venture Capital and Digital Magics: InsurTech, Disposal of Axieme (September 2023)

Incubators:

Deloitte UK: RegTech, Disposal of RegTech business (May 2024)

Fintechs:

Monese: Neo-banking, Disposal of UK consumer business (April 2024)

Klarna: Payments, Disposal of checkout business (June 2024)

Weavr: Open banking, Shutting down of Comma (October 2023)

Block: BNPL, Shutting down of Verse in EU and Clearpay in Spain, France and Italy (August 2023)

Klarna: Open banking, Shutting down of Klarna Kosma (July 2023)

Banks:

Aareal Bank: SaaS, Disposal of equity stake in Aareon (June 2024)

ING: KYC / RegTech, Disposal of CoorpID and Blacksmith KYC (January 2024)

Alior Bank: SME lending, Disposal of Bancovo (November 2023)

ING: Multi-banking platform, Disposal of 85% of Cobase (September 2023)

Saxo Bank: BaaS, Disposal of Saxo Fintech (June 2023)

IPOs:

Zaymer: Microfinance, US$37.5 million Moscow Stock Exchange IPO (April 2024)

Consolidation through acquisitions & partnerships

Deal highlight:

White & Case advised Klarna, the Nordic neo-banking and consumer finance unicorn, on the sale of its virtual shopping business Hero to Bambuser, a Swedish eCommerce tech company.

Market commentary:

In H1 2023, European fintech M&A activity was only down 5%, although there was an 84% decline in transaction sizes (Finextra–September 2023).

Acquisitions:

Robinhood: Crypto, Acquisition of Bitstamp (June 2024)

Fabrick: Open banking, Acquisition of 75% of finAPI (May 2024)

Lukka: Crypto, Acquisition of Coinfirm (May 2024)

BSI: InsurTech, Acquisition of riskine (May 2024)

The Access Group: Finance automation, Acquisition of Lightyear (May 2024)

Corlytics: RegTech, Acquisition of Deloitte UK's RegTech business (May 2024)

Spendesk: SaaS, Acquisition of Okko (April 2024)

Bambuser: e-commerce, Acquisition of Klarna's virtual shopping business Hero (April 2024)

Entrust: Digital ID verification / RegTech, Acquisition of Onfido (April 2024)

Qonto: SaaS, Acquisition of Regate (March 2024)

Levenue: Revenue based finance, Acquisition of MidFunder (March 2024)

Carbon: SME lending, Acquisition of Vella Finance (February 2024)

Lesaka: Data analytics, Acquisition of Touchsides (February 2024)

Trading Technologies: SaaS, Acquisition of Ateo (February 2024)

PragmaGO: Factoring and SME lending, Acquisition of Monevia (February 2024)

team.blue: POS software, Acquisition of helloCash (January 2024)

ieDigital: Digital retirement solutions, Acquisition of ABAKA (January 2024)

Objectway: WealthTech, Acquisition of Nest Wealth (January 2024)

MyInvestor: Price comparison, Acquisition of majority stake in Helloteca (January 2024)

Encompass: KYC / RegTech, Acquisition of CoorpID and Blacksmith KYC (January 2024)

Finax: WealthTech, Acquisition of ETFmatic (January 2024)

GSTechnologies: Payments, Acquisition of 60% of EasySend (November 2023)

Confindo: SME lending, Acquisition of Bancovo (November 2023)

bolttech: InsurTech, Acquisition of Digital Care (October 2023)

Getsafe: InsurTech, Acquisition of Luko’s German business (October 2023)

ieDigital: SaaS, Acquisition of Connect FSS (October 2023)

FE fundinfo: Data analytics, Acquisition of Adjuto (September 2023)

Jung, DMS & Cie: InsurTech, Acquisition of Plug-InSurance from eVorsorge Systems (September 2023)

Blackthorn Finance: Bill-splitting platform, Acquisition of Steven (September 2023)

OPay: Payments, Acquisition of FINJA (September 2023)

Netcompany: Financial software, Acquisition of 20% of Festina Finance (September 2023)

Rauva: Banking, Acquisition of Banco Empresas Montepio (September 2023)

Levenue: Personal financial management, Acquisition of Cake (September 2023)

Clear Junction: Crypto payments, Acquisition of Altalix (September 2023)

Datasite / CapVest: Partners SaaS, Acquisition of MergerLinks (August 2023)

ION: Banking Acquisition of 32% of Cassa di Risparmio di Volterra (July 2023)

Papara: Neo-bankingAcquisition of Rebellion (July 2023)

Corlytics: RegTech, Acquisition of Clausematch (July 2023)

Mergers:

FOCONIS AG, pdv: Financial Software & van den Berg FS: Banking SaaS, Merger (January 2024)

Symphony: RegTech, Financial markets voice analytics JV with Google (November 2023)

Lunate: WealthTech, MENA wealth management technology JV (Alpheya) with BNY Mellon (November 2023)

PragmaGo: Embedded finance, Embedded finance JV with ePlatnosci (November 2023)

Equity investments:

Chetwood Financial: Digital mortgages £500 million equity investment in LendInvest (July 2023)

Restructurings

Deal highlight:

White & Case advised pan-European digital current accounts and money transfers business Monese as well as its global platform-as-a-service business, XYB, on securing new funding and separation into two independent businesses.

Monese & XYB: Digital current accounts and money transfers Demerger (May 2024)

Bitpanda & Bitpanda: Pro / One Trading, Crypto trading Demerger (June 2023)

Equity and debt scale up funding rounds

Deal highlights:

White & Case advised PayPal Ventures, as lead investor, on its participation in the €18 million Series A+ funding round in Pliant, the Berlin-based corporate card platform.

Market commentary:

UK fintech sector received US$2 billion of investment in H1 2024, a 37% decrease from H2 2023 (Innovate Finance–July 2024).

Global fintech sector received US$15.9 billion of investment in H1 2024, a 19% decrease from H2 2023 (Innovate Finance–July 2024).

US fintech sector received the most investment in H1 2024, bringing in US$7.3 billion across 599 deals, with the UK in second place with US$2 billion and 183 deals (Innovate Finance–July 2024).

H1 2024 witnessed a shift toward earlier-stage deals (Seed to Series B), with an average deal value of US$10.2 million, reflecting a return to early-stage investments (Innovate Finance–July 2024).

Africa’s fintech market has secured more than US$2.7 billion in VC funding in the past two years, and the number of fintech startups has grown by 17.7%. Nigeria, Egypt, Kenya and South Africa dominate the market, accounting for 91.2% of funding (Finextra–August 2023).

There are currently 147 active fintechs in Saudi Arabia, a 79% increase from 2021 (Finextra–September 2023).

UK fintech funding dipped in H1 2023, as total cash raised reached US$2.9 billion, a 37% slump compared to H2 2022 (Finextra–July 2023).

In H1 2023, a total of US$27.3 billion was invested in fintech globally, a 14% decline from H2 2022 (Finextra–July 2023).

The European fintech industry bore the brunt of a global drop in fintech funding during H1 2023, declining by more than 50% over H2 2022 (Finextra–July 2023).

Successful fundraisings:

Supercede: InsurTech, Successful US$15 million Series A funding round led by Alven Capital (June 2024)

Numerated: AI-powered modular commercial lending platform, Successful equity investment from Citi (June 2024)

Peak3: InsurTech, Successful US$35 million Series A funding round led by EQT (June 2024)

Zilch: BNPL, Successful £100 million securitised debt financing arranged by Deutsche Bank (June 2024)

Zodia Custody: Digital asset custody Successful equity investment from NAB Ventures (June 2024)

Wealthon: WealthTech, Successful US$12.4 million debt financing from CVI Dom Maklerski (June 2024)

Hawk: RegTech, Successful Series B+ funding round led by Rabobank (June 2024)

Nium: Payments, Successful US$50 million Series E funding round Fintech – Publicly reported deals & situations (June 2024)

Doconomy: ClimateTech, Successful €34 million Series B funding round led by CommerzVentures and UBS (June 2024)

Bondaval: InsurTech, Successful £15 million funding round led by Dawn Capital (May 2024)

FintechOS: FI digitalisation, Successful US$60 million Series B+ funding round led by Molten Ventures (May 2024))

Deedster: ClimateTech, Successful £3.7 million funding round led by Wellstreet (May 2024)

Cloover: ClimateTech, Successful US$114 million, Seed funding round led by Lowercarbon Capital (May 2024)

Colendi: Digital banking, Successful US$65 million funding round led by Citi Ventures, Migros Ticaret, Sepil Ventures, Re-Pie Asset Management, Finberg and Hedef Holding (May 2024)

Vitesse: Payments, Successful US$93 million Series C funding round led by KKR (May 2024)

Cover Genius: InsurTech, Successful US$80 million Series E funding round led by Spark Capital (May 2024)

Fintech Farm: Digital banking, Successful US$32 million Series B and B+ funding round led by Nordstar and Bank of Georgia (May 2024)

Monzo: Digital banking, Successful US$190 million funding round led by Capital G, Hedosophia and GIC (May 2024)

Simplifai: InsurTech, Successful funding round led by Idékapital (May 2024)

Abound: Consumer credit, Successful £800 million debt and equity funding round led by Citigroup, GSR Ventures and Hambro Perks (May 2024)

United Fintech: Digital transformation platform, Successful equity investment from Danske Bank (May 2024)

SumUp: Payments, Successful €1.5 billion funding round led by Goldman Sachs (May 2024)

Lunar: Digital banking, Successful €24.1 million funding round (May 2024)

Pliant: Card platform, Successful €18 million Series A+ funding round led by PayPal Ventures (April 2024)

Flatpay: Payments, Successful €45 million Series B funding round led by Dawn Capital (April 2024)

Finmid: Embedded finance, Successful €35 million funding round led by Blossom Capital, Earlybird VC and Max Tayenthal (April 2024)

Hokodo: Payments, Successful €100 million debt funding round, sourced from Viola Credit (April 2024)

Brim Financial: Credit-card-as-a-service, Successful US$85 million Series C funding round led by EDC Investments (April 2024)

Midas: WealthTech, Successful US$45 million Series A funding round led by Portage Ventures (April 2024)

FloQast: Accounting technology, Successful US$100 million Series E funding round led by ICONIQ growth (April 2024)

Bunq: Neo-banking, Successful US$31 million funding round from existing investors (April 2024)

Scayl: SME and consumer financing platform, Successful €100 million Series A funding round led by (undisclosed) investors (April 2024)

Integrum ESG: ESG WealthTech, Successful £100,000 investment from Industrial Thought (April 2024)

Moove: Automobile finance, Successful US$100 million Series B funding round led by Uber Technologies, Mubadala Investment, The Latest Ventures, Africinvest, Palm Drive Capital, Triatlum Advisors and Future Africa (March 2024)

TUUM: Core banking platform, Successful Series B+ funding round led by Citi Ventures (March 2024)

PPRO: Payments, Successful €80 million funding round led by Eurazeo, HPE Growth, Sprints, PayPal Ventures, J.P. Morgan, Citi Ventures and BlackRock (March 2024)

Perfios: B2B SaaS, Successful US$80 million funding round led by Teachers’ Venture Growth (March 2024)

Monzo: Digital banking, Successful US$430 million funding round led by CapitalG, Hongshan Capital, Google Ventures, Tencent and Passion Capital (March 2024)

FundGuard: AI fund management, Successful US$100 million Series F funding round led by Key1 Capital (March 2024)

HeavyFinance: ClimateTech, Successful €50 million funding round led by European Investment Fund and InvestEU (March 2024)

Lizy: Automotive finance, Successful €11.5 million funding round led by Alychlo, D’Ieteren, and the Flemish Welfare Fund (February 2024)

Napier AI: RegTech, Successful £45 million funding round led by Crestline Investors (February 2024)

FINOM: SME finance, Successful €50 million Series B funding round led by General Catalyst and Northzone (February 2024)

Navro: Embedded payments, Successful US$14 million Series B funding round led by Bain Capital, Unusual Ventures and Motive Partners (February 2024)

Ta-da: Crypto infrastructure, Successful (undisclosed quantum) funding round led by KuCoin Ventures (February 2024)

ALT21: FX hedging, Successful US$21 million pre-series A funding round led by (undisclosed) investors (February 2024)

Pulsate: Mobile banking technology, Successful US$7.7 million Series A funding round led by TruStage Ventures and Curql Collective (February 2024)

Pennylane: Accounting technology, Successful €40 million Series C funding round led by Sequoia Capital and DST Global (February 2024)

TUUM: Core banking platform, Successful €25 million Series B funding round led by CommerzVentures (February 2024)

MTN Fintech: Payments, Successful US$200 million funding round led by Mastercard (February 2024)

Embat: Digital treasury, Successful US$16 million funding round led by Creandum (February 2024)

Spektr: RegTech, Successful €5 million Seed funding round led by Northzone, Seedcamp and PreSeed Ventures (February 2024)

Fordefi: Crypto wallet, Successful US$10 million Seed+ funding round led by Electric Capital (February 2024)

Portal: Crypto wallet, Successful US$34 million Seed funding round led by Coinbase Ventures, Arrington Capital, OKX Ventures and Gate.io (January 2024)

Mesh: Embedded finance, Successful funding round led by PayPal Ventures (payment made in form of PayPal’s US$-denominated stablecoin) (January 2024)

Kuda: Digital banking, Successful US$20 million funding round from (undisclosed) investors (January 2024)

Finoa: Crypto custody, Successful US$15 million funding round led by Maven 11 and Balderton (January 2024)

Kriya: B2B BNPL, Successful £50 million debt financing from Viola Credit (January 2024)

Sygnum Bank: Crypto banking, Successful US$40 million financing round led by Azimut (January 2024)

CryptoSafe: Crypto cybersecurity, Successful US$20 million funding round through crowdfunding (January 2024)

GetirFinans: Mobile banking, Successful US$25 million funding round led by Crankstart Foundation (January 2024)

Billink: BNPL, Successful €29.5 million funding round led by Varengold Bank (January 2024)

10x Banking Technology: BaaS, Successful US$50 million funding round led by JPMorgan Chase and BlackRock (January 2024)

Pliant: Cards-as-a-Service, Successful €33 million Series A+ funding round led by Molten Ventures, SBI Investment, Alstin Capital and Motive Ventures (January 2024)

Carmoola: Automotive finance, Successful £15.5 million funding round led by QED Investors, VentureFriends, InMotion Ventures (Jaguar Land Rover), AlleyCorp and u.ventures (January 2024)

Hyperexponential: InsurTech, Successful US$73 million Series B funding round led by Battery Ventures (January 2024)

Unbox: WealthTech, Successful €12 million Series A funding round led by HSBC Asset Management (January 2024)

ZILO: WealthTech, Successful £25 million Series A funding round led by Fidelity International Strategic Ventures and Portage (January 2024)

MyInvestor: Neo-banking, Successful €45 million Series C funding round led by Nortia Capital (January 2024)

Bumper: Automotive finance, Successful €46 million Series B funding round led by Autotech Ventures and Shell Ventures (January 2024)

Tabby: BNPL, Successful US$700 million debt funding round led by J.P. Morgan (December 2023)

Tabby: BNPL, Successful US$50 million Series D+ funding round led by Hassana Investment (December 2023)

Updraft: Consumer credit, Successful £22 million equity and debt funding round led by Quilam Capital (December 2023)

Tamara: BNPL, Successful US$340 million Series C funding round led by Sanabil Investments and SNB Capital (December 2023)

Meniga: Personal finance management, Successful €15 million Series D funding round led by Groupe BPCE, Credito Agricola and Omega EHF (December 2023)

Nearpay: Payments, Successful US$14 million Series A funding round led by Sanabil Investments (December 2023)

Aria: Invoice financing, Successful €15 million funding round led by 13books Capital (December 2023)

SumUp: Payments, Successful €285 million debt and equity funding round led by Sixth Street Growth and Bain Capital Tech Opportunities (December 2023)

GFO-X: Digital asset exchange, Successful US$30 million Series B funding round led by M&G Investments (December 2023)

Scalable Capital: WealthTech, Successful €60 million Series E+ funding round led by Balderton Capital (December 2023)

Pontera: Trade technology, Successful US$60 million funding round led by ICONIQ Growth (December 2023)

QuantoPay: Payments, Successful €150 million funding round (November 2023)

Enfuce: Payments, Successful €8.5 million Series C+ funding round led by Vitruvian Partners, Visa and Maki.vc (November 2023)

Paysend: Payments, Successful US$65 million funding round led by Mastercard, Hermes GPE, One Peak Partners and Infravia Growth Capital (November 2023)

TRIVER: SME / working capital finance, Successful £20 million funding round led by Avellinia Capital (November 2023)

Silverflow: Payments, Successful €15 million funding round led by Global Paytech Ventures (November 2023)

Defacto: SME lending, Successful €10 million Series A+ funding round led by Citi Ventures (November 2023)

Credix: Decentralised debt funding platform, Successful US$60 million funding round led by Rockaway Blockchain Fund (November 2023)

Fnality: Payments, Successful £77.7 million Series B funding round led by Goldman Sachs and BNP Paribas (November 2023)

Imprint: Payments, Successful US$75 million Series B funding round led by Ribbit Capital (November 2023)

Monument Bank: Neo-banking, Successful £40 million Series B funding round led by Dubai Investments (November 2023)

Qomodo: Payments, Successful €34.5 million Seed funding round led by Fasanara Capital (November 2023)

Tabby: BNPL, Successful US$200 million Series D funding round led by Wellington Management (November 2023)

Atom Bank: Digital banking, Successful £100 million funding round led by Toscafund, BBVA and Infinity Investment Partners (November 2023)

Zilch: BNPL, Successful equity funding round led by eBay Ventures (October 2023)

Railsr: Embedded finance, Successful £20 million funding round led by D Squared Capital and Moneta Venture Capital (October 2023)

multifi: SME lending, Successful £10 million debt funding round led by Fasanara Capital (October 2023)

Nova Credit: Data analytics, Successful US$43 million Series C funding round led by Canapi Ventures (October 2023)

iwoca: SME lending, Successful £200 million debt funding round led by Barclays Bank and Varde Partners (October 2023)

Cash Plus: Payments, Successful €57 million funding round led by Mediterrania Capital Partners (October 2023)

Upvest: Digital investment platform, Successful €30 million funding round led by BlackRock, ABN AMRO Ventures, Bessemer Venture Partners, Notion Capital, Earlybird, 10x Capital and HV Capital (October 2023)

Untangled Finance: Decentralised finance, Successful US$13.5 million funding round led by Fasanara Capital (October 2023)

Kennek: SaaS, Successful US$12.5 million funding round led by HV Capital (October 2023)

Brite Payments: Payments, Successful US$60 million funding round led by Dawn Capital (October 2023)

Stitch: Payments, Successful US$25 million Series A+ funding round led by Ribbit Capital (October 2023)

Perenna: Mortgage lending, Successful US$52 million funding round led by Silverstripe Investment Management (September 2023)

Apron: SME invoice processing software, Successful US$15 million Series A funding round led by Index Ventures (September 2023)

Fleximize: SME lending, Successful £136 million securitised funding round led by Goldman Sachs and Citibank (September 2023)

Curve: Payments, Successful £58 million Series C+ funding round led by Britannia, Outward Venture Capital, IDC Ventures, Cohen Circle and Cercano Management (September 2023)

Payflow: Payroll finance, Successful €20 million debt funding round led by BBVA Spark (September 2023)

Erguvan: ESGTech, Successful Seed funding round led by Emirates NBD (September 2023)

HyperJar: Pre-paid debit card app for kids, Successful US$24 million Series A funding round led by Susquehanna Private Equity (September 2023)

Fipto: DLT treasury management, Successful €15 million Seed funding round led by Serena Capital, Purple. and Motier Ventures (September 2023)

Swan: BaaS, Successful €37 million Series B funding round led by Lakestar (September 2023)

Form3: Payments / API connectivity, Successful funding round led by Visa (September 2023)

Zopa: Digital banking, Successful £75 million (internal) funding round led by Silverstripe (September 2023)

ThetaRay: RegTech, Successful US$57 million funding round led by Portage Ventures (September 2023)

Komgo: Trade finance software, Successful funding round led by Citi Ventures and Emirates NBD (September 2023)

Finiata: SME lending, Successful €20 million equity funding round led by Fasanara Capital (August 2023)

Zanifu: SME lending, Successful US$11.2 million pre-Series A debt & equity funding round led by Beyond Capital Ventures and Variant Investments (August 2023)

Fineos: InsurTech, Successful €24 million funding round led by (unnamed) institutional investors, Fintech – Publicly reported deals & situations (August 2023)

Tradeshift: Supply chain finance, Successful US$35 million funding round led by HSBC (August 2023)

Bunq: Neo-banking, Successful €44.5 million funding round led by Pollen Street Capital (July 2023)

Tractable: InsurTech, Successful US$65 million Series E funding round led by SoftBank Vision Fund 2 (July 2023)

Tandem: Neo-banking, Successful £20 million funding round led by Quilam Capital (July 2023)

LendInvest: Mortgage lending, Successful £500 million equity investment from Chetwood Financial (July 2023)

Komgo: Trade finance software, Successful equity funding round led by Santander (June 2023)

Bitpanda: Crypto trading, Successful €30 million funding round led by Valar Ventures (June 2023)

Splitting at the seams

Market commentary:

63% of tech startups fail – 75% of VC-backed fintechs fail (PYMNTS–December 2023).

Close to half of UK fintechs fear that they may not make it to the end of the year due to ongoing economic challenges (findsTech–July 2023).

Chase: UK, Ban of crypto-related transactions from mobile app (September 2023)

Bank for International Settlements: US, Collaboration with seven central banks on exploration of tokenisation of cross-border payments (April 2024)

Bank for International Settlements: US, Warning of metaverse placing new demands on payment services which may be better met by central bank digital currencies (February 2024)

Basel Committee on Banking Supervision: Pan-European, Proposals for banks to disclose exposure to crypto assets (October 2023)

Top-down support for fintech

Governments:

Microsoft: AI, Acquisition of US$1.5 billion interest in G42, with support of U.S. and UAE governments (April 2024)

Folketrygdfondet: SaaS, Participation in €82 million funding round in Ageras (February 2024)

Flemish Welfare Fund: Automotive finance, Participation in €11.5 million funding round in Lizy (February 2024)

European Investment Fund and InvestEU: ClimateTech, Participation in €50 million funding round in HeavyFinance (January 2024)

Fintech Growth Fund: Fintech Launch of new fund for Series C rounds and above, with ticket size of £10 million to £100 million (August 2023)

Regulators:

UK Financial Conduct Authority: Investigations into competitive implications of BigTech in financial services (April 2024)

Bank of England and UK Financial Conduct Authority: Consultation paper for Digital Securities Sandbox (April 2024)

Qatar Central Bank: Instructions for the Loan-Based Crowdfunding Regulation (October 2023)

Politicians:

Tony Blair Institute for Global Change: Call on Labour Party to leverage fintech sector as catalyst for UK economic growth, opportunity and inclusivity (April 2024)

UK Labour Party: Aim of delivery of next phase of open banking and embrace of securities tokenisation (February 2024)

UK Treasury: Rejection by all-party parliamentary committee’s proposals for consumer trading in unbacked crypto to be regulated as gambling (July 2023)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: 5-year fintech funding landscape - Global (PDF)

View full image: 5-year fintech funding landscape - Global (PDF)

View full image: 5-year fintech funding landscape - UK (PDF)

View full image: 5-year fintech funding landscape - UK (PDF)