Green hydrogen will play important roles in Africa's transition to renewable energy and as an exportable commodity. But is the current focus on the areas that will deliver the most value for Africa and its people? Carina Radford and Alex Field explain green hydrogen's potential for diversifying the continent's industrial base and contributing to bridging Africa's energy deficit—as well as for growing exports.

Disputes related to climate change are growing steadily, but most so far have been in North America, Europe and Australia. Markus Burianski and Federico Parise Kuhnle explain why these will likely ramp up in Africa, too. Disputes could involve liability and compensation for damages caused by climate change, how environmental regulations aimed at mitigating climate change are implemented and enforced, and investment disputes.

Sustainable finance is a perennially important topic in Africa, as is sovereign debt. Olga Fedosova and Max Turner combine these two, explaining Gabon's Blue Bond issuance (the first on the African mainland), exploring lessons from that innovative and important debt-for-nature swap, and outlining how such swaps might be deployed elsewhere in Africa.

In our third article, Marcus Booth and James Ateh interview Sam Senbanjo, Managing Director at private equity fund A.P. Moller Capital, about his experiences in Africa. The interview covers A.P. Moller Capital activities in Africa (including its approach to ESG), prospects for African PE generally and some very practical pointers for those considering investing on the continent.

The Koeberg Nuclear Power Station in South Africa is currently the only nuclear power station in Africa, but that is changing. The International Atomic Energy Agency (IAEA) forecasts between a five-fold and ten-fold increase in African nuclear power generation by 2050, compared to 2022. Ximena Vasquez-Maignan explains the process defined by the IAEA for developing new nuclear power stations, and the challenges involved.

Our final article examines exciting new oil & gas discoveries in Namibia. These are of a scale that could transform Namibia's economy and the livelihoods of its people, propelling the country to middle-income status. Gary Felthun and Tariq Kajee, collaborating with Irvin Titus of leading Namibian law firm Koep, explore implications for foreign direct investment into Namibia—especially into green hydrogen and mining projects.

Our eleventh edition of Africa Focus, delves into key aspects of Africa’s shift towards renewable energy and sustainable economic growth

Green hydrogen in Africa: A continent of possibilities?

There is huge interest in the development of green hydrogen projects in Africa, building on the continent's vast potential for renewable energy. But are these the right projects to achieve success, both for investors and for African populations?

A new wave of African climate change disputes on the horizon

Africa's heavy reliance on fossil fuels for economic growth, set against the backdrop of strict environmental regulations and emissions-reduction targets, creates a perfect storm of factors that could give rise to climate change-related disputes in Africa.

Debt-for-nature swaps: A viable alternative for vulnerable economies amid global challenges

Debt-for-nature swaps convert debts of low- and middle-income countries, unable to service external debts, into commitments related to nature. In the face of recent geopolitical tensions, economic challenges and growing environmental concerns, DFNSs offer a promising alternative to traditional financing sources when access to international capital markets or commercial loans is limited.

In an exclusive interview, Marcus Booth and James Ateh discuss Africa's infrastructure, renewable energy and investment landscape with Sam Senbanjo, A.P. Moller Capital.

Africa’s quest for universal electricity access and net- zero through small modular reactors

Africa needs to significantly increase its electricity production to ensure universal access to its expanding population. It also needs to achieve net-zero emissions by 2050. Small modular reactors (SMRs) offer a potentially accessible and sustainable solution, but financing and regulatory hurdles must be addressed for widespread adoption.

Namibia's regulatory environment, stable economy and rich mineral resources make it an attractive investment destination in Africa. Investors should view Namibia as a key emerging investment hub on the continent.

Green hydrogen in Africa: A continent of possibilities?

There is huge interest in the development of green hydrogen projects in Africa, building on the continent’s vast potential for renewable energy. But are these the right projects to achieve success, both for investors and for African populations?

As the world continues along the path to energy transition, there is an opportunity for Africa, with its rich and largely untapped renewable energy potential, to become a key player in the growing field of green hydrogen. Hydrogen as an energy source and industrial chemical is not new—however, traditional production methods based around fossil fuels entail significant carbon emissions. Green hydrogen, produced through the electrolysis of water using renewable energy, offers a carbon-neutral alternative. As an energy carrier and fuel, it can help to balance often unpredictable renewable energy sources and decarbonize the power and transportation sectors. Green hydrogen can also play a role in decarbonizing many otherwise carbon-intensive heavy industrial processes (such as steel and cement manufacturing), as well as providing a more environmentally sustainable production method for fertilizers and other chemicals.

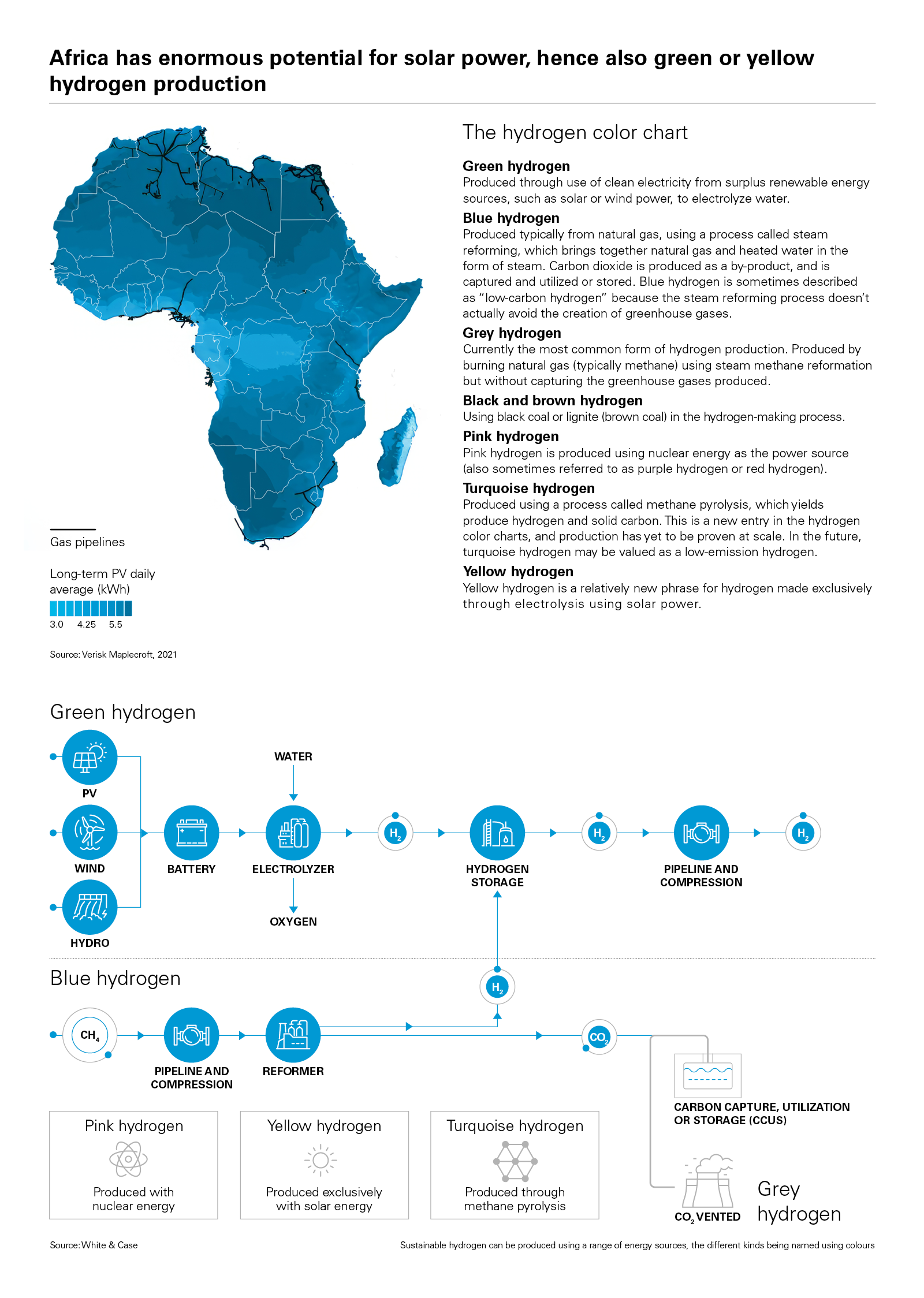

Africa, blessed with some of the world’s greatest and currently undeveloped solar and wind potential, is uniquely positioned to become a major producer of green hydrogen

Focus on green hydrogen in Africa

Significant strides have already been taken to position Africa at the heart of green hydrogen developments. The establishment in 2022 of the Africa Green Hydrogen Alliance between Egypt, Kenya, Mauritania, Morocco, Namibia and South Africa (six of the key countries leading green hydrogen efforts on the continent) was coupled with the launch of the European Union's REPowerEU Plan. This plan, focused on accelerating renewable energy development, includes targets to import up to ten million tons per year of green hydrogen, much of it from Africa.

Africa is uniquely positioned to become a major producer of green hydrogen. The continent is blessed with some of the world's greatest solar and wind potential, much of which is currently undeveloped. The International Energy Agency estimates that Africa has 60 percent of the world's best solar resources, but so far accounts for only 1 percent of global solar generation capacity.

The continent is also facing a massive energy gap—roughly 600 million Africans currently lack access to electricity. The rapid population and economic growth anticipated across the continent demands an increased energy supply—by harnessing renewable energy resources for green hydrogen production, countries across the continent could fuel this growth in an environmentally sustainable manner. Countries in Africa also have access to many of the mineral and other resources critical to the green hydrogen production process, such as platinum and platinum group metals for use in fuel cells and other critical minerals key to next-generation technologies.

There is scope for robust exports of African green hydrogen. The European Investment Bank estimates that Africa could have a green hydrogen production capacity exceeding 50 million tonnes per annum by 2035. This production is projected to be economically viable at just €2 per kilogram, which is highly competitive with global oil prices—currently in the region of €90 per barrel. With their close proximity to Europe, countries such as Morocco, Mauritania and Egypt are well positioned to integrate production into the growing European hydrogen pipeline network as part of the European Hydrogen Backbone initiative. Other African nations also have the potential to leverage existing sea transport infrastructure to export derivative products such as green ammonia.

The realization of such export potential could bring an influx of foreign investment and advance development of critical power and water infrastructure across the continent, with benefits across the population. It could also create jobs across the value chain and diversify Africa's economies, supporting the growth of industries covering renewable energy and green hydrogen; derivative products such as green ammonia and other green fertilizers; further semi-finished and industrial products such as green steel and green cement; and the equipment and components necessary for green hydrogen production.

Realizing this vision of Africa as a green hydrogen powerhouse is not without its challenges. One of the most significant hurdles will be the sheer scale of infrastructure development required to support green hydrogen production and export at scale. Many parts of Africa that would be ideal for renewable energy generation remain seriously underdeveloped. Substantial investments will therefore be needed in transmission infrastructure to connect renewable energy sources to production facilities and export hubs. Governments will also need to balance their own broader energy strategy against heavy growth of non-dispatchable renewables, which could strain underdeveloped national transmission grids.

Moreover, the requirement for clean water for hydrogen production poses additional challenges, especially in regions where water resources are already scarce. To address this, some projects are already factoring in desalination as part of their overall design to meet clean water needs. Furthermore, while some countries are well positioned to take advantage of existing gas transportation and export infrastructure, others will need to build this from scratch if they are to access key export markets. These multi-faceted development requirements all add to the capital cost required for large-scale green hydrogen projects and build in substantial project-on-project risks that will need to be carefully managed to ensure their viability and successful implementation.

The political and investment environment across Africa is diverse and often challenging. This variance necessitates careful consideration and management, given the scale of investments required. While export-driven projects have the advantage if selling to hard-currency markets, there may still be a need for domestic subsidies and price support to make certain projects competitive.

Green hydrogen projects need to be developed in order to directly benefit local communities, too. Africa currently contributes only 4 percent of global carbon emissions—it should not be the case that all the benefits of green hydrogen development go to enable continued consumption in wealthy foreign markets, thereby replicating historical resource extraction behaviors that treated Africa as a low-cost provider of primary resources. If green hydrogen development is primarily export-driven, real care will be needed (and governments may have to actively step in) to ensure that energy, infrastructure, and water resources are also put to work for the benefit of the country and local communities more generally.

50m tonnes

The European Investment Bank estimates that Africa could have a green hydrogen production capacity exceeding 50 million tonnes per annum by 2035

Green hydrogen for export – the current focus

Much attention is currently focused on the possibility of producing green hydrogen in Africa for export. A wide range of very large-scale projects has been announced, such as the 15 GW Aman project in Mauritania, the 3 GW Tsau Khaeb project in Namibia and the 4 GW SCZONE project in Egypt. Multiple cooperation agreements between African nations and European partners have also been signed in recent months, such as the announcements in June and July of blended financing vehicles for hydrogen investment in Namibia (SDG Namibia One, a partnership between Namibia's Environment Investment Fund with the Dutch organizations Climate Fund Managers and Invest International, owned by the Dutch Ministry of Finance, targeting €1 billion) and South Africa (SA-H2, established by the governments of South Africa, the Netherlands and Denmark and with the support of FMO, Sanlam InfraWorks, International, the Development Bank of Southern Africa, the Industrial Development Corporation and others, targeting US$1 billion).

Production for export has the advantage of bringing in foreign investment and enabling access to external price support and incentives, as well as opportunities for concessional and ECA-financing—coupled with relatively cheap solar generation at scale; this provides a strong basis for African projects to achieve vital cost-competitiveness. However, there are challenges. The significant multi-faceted development required to bring these projects to fruition will drive up capital costs and tariffs. Furthermore, African nations are not alone in targeting a lucrative export market—leaving aside competition between nations on the continent, countries such as Chile are also aiming to become leaders in hydrogen export, competing on price for the same export markets with the same product. It also remains to be seen whether the large-scale planned projects will come to fruition—these are many times larger than the relatively modest pilot projects currently coming on-stream, and are being developed against a generally constrained supply environment for key components for green hydrogen development and a background of high inflation.

Captive green hydrogen projects – an alternative path?

An alternative path to export projects could be the development of captive green hydrogen initiatives. These projects may initially be smaller in scale and focus on meeting domestic industrial needs. This might even include local airfields producing hydrogen for aviation fuel, as hydrogen-powered aircraft gain traction. Such projects align with domestic industrial development and may offer a more sustainable growth model. The Green Hydrogen Strategy and Roadmap for Kenya launched in September exemplifies this approach, putting much focus toward the production of domestic alternatives to imported hydrogen commodities, such as fertilizer or methanol, with the aim of mitigating supply risks and market price volatility to the benefit of the domestic economy.

In the longer term, green energy and green hydrogen could form the base for domestic-focused industrial hubs, supporting industrial development wherever there is sun, wind and water to match growing population and economic demand in a manner that is "green" from the beginning. As the prices for the technology involved in green hydrogen production are steadily driven down by export development, this could provide a viable opportunity for countries with substantial renewable energy- generating capacity that are not currently well positioned to tap into foreign export markets. A focus on more semi-finished and downstream products (such as green steel or green cement) could also provide a viable avenue for long-term growth, positioning African green hydrogen economies further up the value chain.

A key challenge for such industrial development will be achieving cost competitiveness, working from a more limited market and in an environment where it is more challenging to leverage hard currency financing and external price support. Availability of appropriate financing will be key, particularly for the medium-sized local firms critical to developing industrial hubs—such firms are not always well-catered for by the existing financing instruments in the green hydrogen space, given their smaller transaction volumes and domestic customer base.

There are many opportunities for green hydrogen projects across Africa, supporting the growth of economies and helping drive the continent’s energy transition

Distinct opportunities

Certainly, there are many opportunities for the development of green hydrogen projects across the continent of Africa, supporting the growth of major green hydrogen economies and playing a key role in the energy transition, both for Africa and the wider world. It would be incorrect to assume though that there is only one right path that all countries in Africa could (or should) follow—development will inevitably need to build on and be guided by the specifics of local markets and conditions, following a distinct path in distinct locations. There is a clear focus on export development in the emerging frontrunner markets in north Africa, with a case for direct linkage into growing European pipeline infrastructure, and for sea transport from southern Africa. However, this cannot be the only focus, and other countries may need to find alternative avenues for development if they are to benefit. This could take the form of domestic-focused production aimed at the substitution of imports, the broader development of green industries (such as green steel or green cement) and industrial hubs built from the ground up around abundant renewable energy, or opportunities for "blue" hydrogen incorporating carbon capture in countries with significant and developed oil & gas resources.

Realizing this huge potential will be challenging, with projects crossing a range of sectors and requiring significant coordination and extensive financing. The regulatory landscape for green hydrogen development will be complex— green hydrogen is itself an emerging industry, and the multi-faceted development required to support projects in Africa will inevitably touch on a range of other sectors (including power generation and transmission, water, industrial processes, transportation and export) with their own regulatory requirements and practices. Future-proofing projects to maintain compliance with ever-developing "green" standards in export markets will also be a key and ongoing challenge. Nevertheless, as projects progress and African nations continue to explore and expand their capabilities, the likelihood of an economic and environmental transformation for the continent and beyond only increases.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

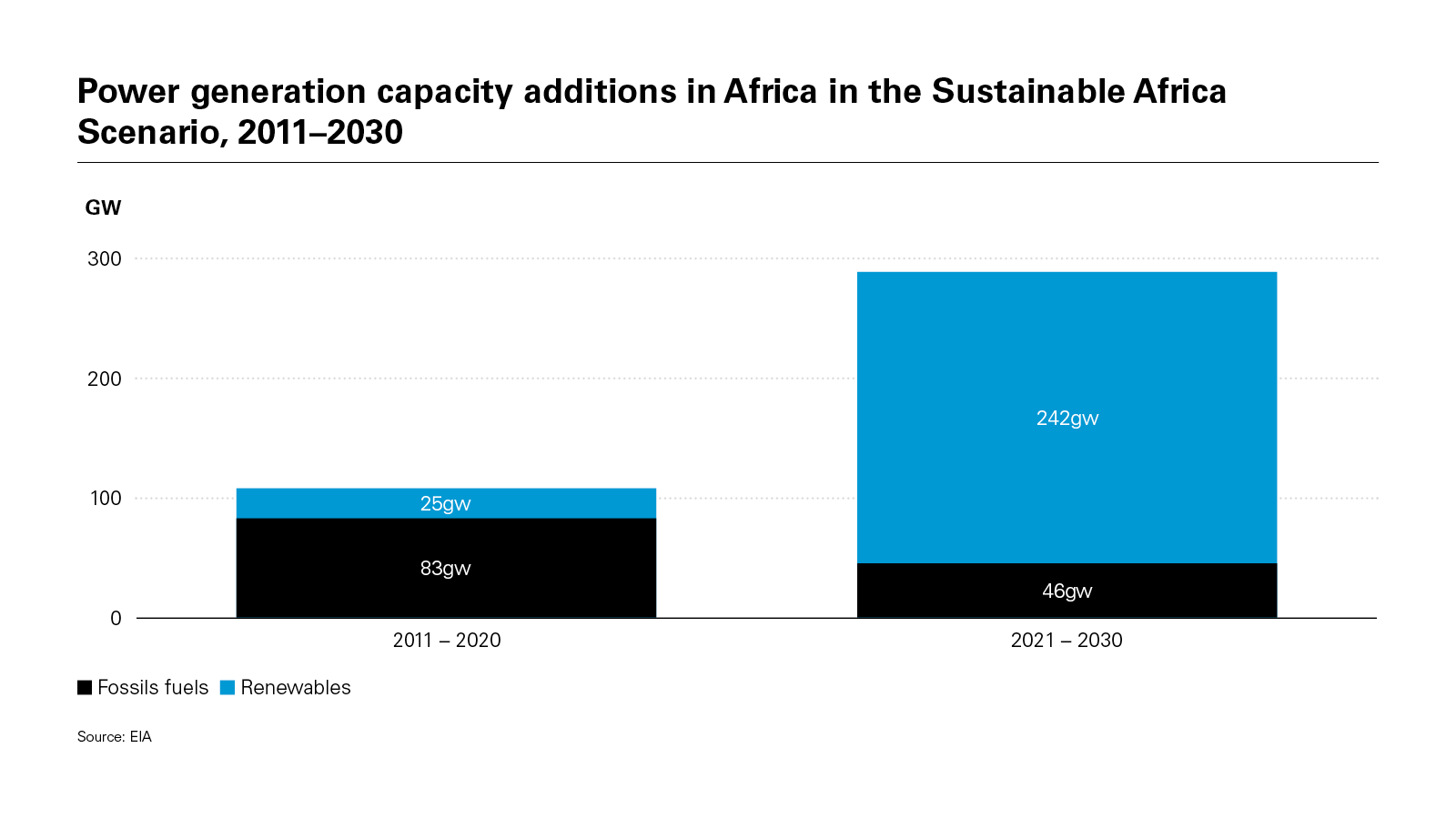

View full image: Power generation capacity additions in Africa in the Sustainable Africa Scenario, 2011–2030 (PDF)

View full image: Power generation capacity additions in Africa in the Sustainable Africa Scenario, 2011–2030 (PDF)

View ful image: Africa has enormous potential for solar power, hence also green or yellow hydrogen production (PDF)

View ful image: Africa has enormous potential for solar power, hence also green or yellow hydrogen production (PDF)